NOTES TO THE FINANCIAL STATEMENTS

1

Reporting Entity

1.1 Corporate information

Bank of Ceylon (“The Bank”) is a

Government-owned bank domiciled

in Sri Lanka, duly incorporated on 1

August 1939 under the Bank of Ceylon

Ordinance No. 53 of 1938. It is a licensed

commercial bank established under

the Banking Act No. 30 of 1988 and

amendments thereto. The Registered

Office of the Bank is situated at “BoC

Square”, No. 01, Bank of Ceylon

Mawatha, Colombo 01, Sri Lanka. The

debentures issued by the Bank are listed

on the Colombo Stock Exchange. The

staff strength of the Bank as at

31 December 2023 was 8,579 (2022- 8,209).

1.2 Consolidated financial statements

The Consolidated Financial Statements

are prepared as at and for the year

ended 31 December 2023 comprise

the Bank (“Parent”), its Subsidiaries

(together referred to as the “Group”

and individually as (“Group Entities”)

and the Group’s interests in its Associate

companies. The Financial Statements

of the companies in the Group have a

common financial year which ends on

31 December, except the Associate

companies, Transnational Lanka Records

Solutions (Private) Limited and Ceybank

Asset Management Limited. The Bank is

the ultimate parent of the Group.

1.3 Principal activities

1.3.1 Bank

The principal activities of the Bank

during the year were, personal banking,

corporate banking, development

banking, off-shore banking, trade

financing, lease financing, primary

dealing, investment banking and

wealth management, treasury

operations, correspondent banking and

money remittances, Islamic banking,

bancassurance, pawning, credit card

facilities, foreign currency operations and

other financial services.

1.3.2 Subsidiaries

The principal activities of the Subsidiaries of the Bank are as follows:

Name of the Company

Principal Business Activities

Property Development Limited Own, maintain and manage, develop and sustain the

utility and value of the Bank of Ceylon head office

building.

Merchant Bank of Sri Lanka &

Finance PLC

Leasing, hire purchase, corporate and retail credit

facilities, corporate advisory services, capital

market operations, margin trading, microfinancing,

agricultural credit facilities, real estate, pawning,

Islamic finance and accepting deposits.

Bank of Ceylon (UK) Limited

Authorised commercial bank by the Prudential

Regulation Authority and regulated by the Financial

Conduct Authority in England and Wales, engages

in retail and corporate banking, treasury operations,

correspondent banking services and trade financing

activities.

BoC Property Development &

Management (Private) Limited

Renting of office space of BoC Merchant Tower in

Colombo 03 and Ceybank House in Kandy.

BoC Travels (Private) Limited

Engages in travel related services.

Hotels Colombo (1963) Limited Provides hotel services.

Ceybank Holiday Homes

(Private) Limited

Managing, operating and maintaining of travel rests/

hotels/rest houses/guest houses.

MBSL Insurance Company

Limited

Carrying on insurance business, both life and non-life

insurance.

BoC Management & Support

Services (Private) Limited

Not in operation.

1.3.3 Associates

The principal activities of the Associates of the Bank are as follows:

Name of the Company

Principal Business Activities

Ceybank Asset Management

Limited

Management of unit trust funds and other institutional

and private portfolios.

Lanka Securities (Private)

Limited

Registered stock broker, trading in equity and

debt securities, equity debt security brokering and

undertaking placement of equity and debt securities.

Transnational Lanka Records

Solutions (Private) Limited

Renting buildings and hiring other assets.

Southern Development

Financial Company Limited

Not in operation and in the process of liquidation.

BoC Management & Support Services (Private) Limited (MSS) has not carried out its

core business activities since 2007. Southern Development Financial Company Limited

(SDFCL) is also not in operations. The Board of Directors of SDFCL has decided to

wind-up the company and it is in the process of liquidation.

2

Directors’ responsibility for

financial statements

2.1 Preparation and presentation of

the financial statements

The Board of Directors is responsible

for the preparation and presentation of

the Financial Statements of the Bank

and its Subsidiaries and Associates in

compliance with the requirements of

the Bank of Ceylon Ordinance No. 53

of 1938 and its amendments, Banking

Act No. 30 of 1988 and its amendments

thereto and Sri Lanka Accounting

Standards (SLFRSs and LKASs). These

Financial Statements comprise.

• Statement of Profit or Loss

• Statement of Comprehensive Income

• Statement of Financial Position

• Statement of Changes in Equity

• Statement of Cash Flows

• Notes to the Financial Statements

2.2 Approval of financial statements

The Financial Statements for the

year ended 31 December 2023 were

authorised for issue on 27 February 2024

by the Board of Directors.

3

Basis of preparation

3.1 Statement of compliance

The Consolidated Financial Statements

of the Group and the separate Financial

Statements of the Bank have been

prepared in accordance with Sri Lanka

Accounting Standards comprising Sri

Lanka Financial Reporting Standards

(SLFRSs) and Sri Lanka Accounting

Standards (LKASs) laid down by the

Institute of Chartered Accountants of Sri

Lanka (together referred to as SLFRSs in

these Financial Statements).

The preparation and presentation

of these Financial Statements are in

compliance with the requirements of

the Bank of Ceylon Ordinance No. 53 of

1938, the Banking Act No. 30 of 1988,

the Companies Act No. 07 of 2007 and

regulatory guidelines issued by the

Central Bank of Sri Lanka (CBSL). The

Group has prepared Financial Statements

which comply with SLFRSs applicable

for the year ended 31 December 2023,

together with the comparative year data

as at and for the year ended

31 December 2022, as described in the

accounting policies.

The formats used in the preparation and

presentation of the Financial Statements

and the disclosures made therein also

comply with the specified formats

prescribed by the Central Bank of Sri

Lanka (CBSL) in the Circular No. 02 of

2019 on “Publication of Annual and

Quarterly Financial Statements and Other

Disclosures by Licensed Banks”.

3.2 Basis of measurement

The Financial Statements have been

prepared on the basis of historical cost

convention and no adjustments have

been made for inflationary factors which

has been applied on a consistent basis,

except for the following:

• Derivative financial instruments are

measured at fair value (Notes 26

and 41)

• Financial assets recognised through

profit or loss – measured at fair value

(Note 27)

• Financial assets measured at fair

value through other comprehensive

income (Note 30)

• Owner-occupied freehold land

and buildings and buildings on

leasehold lands are measured at

revalued amount less any subsequent

accumulated depreciation and

impairment losses (Note 34)

• Defined benefit obligations are

actuarially valued and recognised

at the present value of the defined

benefit obligation less total of the fair

value of plan assets (Note 48)

• Cash flow hedge reserve, accounted

as per the hedge accounting (Note 53)

3.3 Presentation of financial

statements

Items in the Statement of Financial

Position of the Bank and the Group

are grouped by nature of such item

and presented broadly in order of their

relative liquidity and maturity pattern. An

analysis regarding recovery or settlement

within 12 months after the reporting

date (current) and more than 12 months

after the reporting date (non-current)

is presented in Note 60 – “Maturity

Analysis of Assets and Liabilities”.

3.3.1 Functional and presentation

currency

Items included in the Financial

Statements are measured and presented

in Sri Lankan Rupees (“LKR”) which is

the functional currency of the primary

economic environment in which the Bank

operates.

3.3.2 Accrual basis of accounting

The Financial Statements, except for

information on Statement of Cash Flows

have been prepared following the accrual

basis of accounting.

3.3.3 Offsetting

Financial assets and financial liabilities are

generally reported gross in the Statement

of Financial Position. They are only offset

and reported net when, in addition

to having an unconditional legally

enforceable right to offset the recognised

amounts without being contingent on a

future event, the parties also intend to

settle on a net basis in all of the following

circumstances:

• The normal course of business.

• The event of default.

• The event of insolvency or bankruptcy

of the Bank/Group and/or its

counterparties.

Income and expenses are not offset in

the Statement of Profit or Loss unless

required or permitted by any accounting

standard or interpretation and as

specifically disclosed in the accounting

policies of the Group.

3.3.4 Comparative information

The comparative information is provided

in narrative and descriptive nature,

if it is relevant to understand the

current period’s Financial Statements

and reclassified wherever necessary

to conform to the current year’s

presentation.

3.3.5 Materiality and aggregation

In compliance with LKAS 1 –

“Presentation of Financial Statements”,

each material class of similar items are

presented separately in the Financial

Statements. Items of dissimilar nature or

functions are presented separately unless

they are immaterial.

3.3.6 Rounding

The amounts in the Financial Statements

have been rounded-off to the nearest

Rupees thousands, except where otherwise

indicated as permitted by the LKAS 1 –

“Presentation of Financial Statements”.

3.3.7 Statement of cash flows

The Statement of Cash Flows is prepared

by using the “Indirect Method”

in accordance with the LKAS 7 –

“Statement of Cash Flows” whereby the

profit is adjusted to derive the cash flows

from operating activities. Cash and cash

equivalents comprise cash in hand, other

short term highly liquid investments with

maturity less than seven days from date

of acquisition and bank overdrafts.

3.3.8 Use of material accounting

judgements, estimates and

assumptions

The preparation of the Financial

Statements requires Management to

exercise judgements, estimates and

assumptions that affect the application

of accounting policies and the reported

amounts of assets, liabilities, income

and expenses. Actual results may differ

from these estimates. The judgements,

estimates and assumptions are based

on historical experience and various

other factors that are believed to be

reasonable under the circumstances and

reviewed on an ongoing basis. Revisions

to accounting estimates are recognised

in the period in which the estimates

are revised and/or in future periods if

the revision affects future periods too.

In the process of applying the Group’s

accounting policies, Management

has made the following judgements,

estimates and assumptions, which

have the most significant effect on the

amounts recognised in the Financial

Statements. The accounting policies

which are most sensitive to the use of

judgements, estimates and assumptions

are specified below.

3.3.8.1 Going concern

The Management has made an

assessment on the Group’s ability to

continue as a going concern and is

satisfied that it has the resources to

continue in business for the foreseeable

future. Furthermore, management is

not aware of any material uncertainties

that may cast significant doubt upon

the Group’s ability to continue as a

going concern. Therefore, the Financial

Statements continue to be prepared on

the going concern basis. Accordingly,

the Management satisfied itself that the

going concern basis is appropriate.

3.3.8.2 Commitment and contingent

liabilities

All discernible risks are accounted for

in determining the amount of all known

and measurable liabilities. Contingent

liabilities are possible obligations

whose existence will be confirmed

only by uncertain future events or

present obligations where the transfer

of economic benefit is not probable or

cannot be reliably measured. Contingent

liabilities are not recognised in the

Statement of Financial Position but are

disclosed unless its considered remote

that the Group will be liable to settle the

possible obligation.

3.3.8.3 Fair value of financial

instruments

Fair value is the price that would

be received to sell an asset or paid

to transfer a liability in an orderly

transaction between market participants

at the measurement date. Where the

classification of a financial asset or

liability results in it being measured

at fair value, wherever possible, the

fair value is determined by reference

to the quoted bid or offer price in

the most advantageous active market

to which the Group has immediate

access. An adjustment for credit risk is

also incorporated into the fair value as

appropriate. Fair value for a net open

position that is a financial liability quoted

in an active market is the current offer

price, and for a financial asset the bid

price, multiplied by the number of units

of the instrument held or issued. Where

no active market exists for a particular

asset or liability, the Group uses a

valuation technique that include the

use of mathematical models to arrive

at the fair value, including the use of

transaction prices obtained in recent

arm’s length transactions, discounted

cash flow analysis, option pricing models

and other valuation techniques based

on market conditions and risks existing

at reporting date. In doing so, fair value

is estimated using a valuation technique

that makes maximum use of observable

market inputs and places minimal

reliance upon entity-specific inputs.

The best evidence of the fair value of a

financial instrument at initial recognition

is the transaction price (i.e. the fair value

of the consideration given or received)

unless the fair value of that instrument

is evidenced by comparison with other

observable current market transactions

in the same instrument (i.e. without

modification or repackaging) or based

on a valuation technique whose variables

include only data from observable

markets. When such evidence exists, the

Group recognises the difference between

the transaction price and the fair value

in profit or loss on initial recognition

(i.e. on day one). The valuations of

financial instruments are described

comprehensively in Note 63.

3.3.8.4 Impairment charge for loans

and advances

The measurement of impairment charge

under SLFRS 9- “Financial Instruments”

requires judgement by Management

in identification and estimation of the

amount and timing of future cash flows

when determining an impairment charge

for loans and advances. Accordingly, the

Group reviews its individually significant

loans and advances at each reporting

date to assess whether an impairment

charge should be provided in the

Statement of Profit or Loss. In particular,

the Management’s judgement is required

in identification and estimation of the

amount and timing of future cash flows

when determining the impairment loss.

In estimating these cash flows, the Group

makes judgements about the borrower’s

financial position, the net realisable

value of collateral and other related

factors. These estimates are based on

assumptions about a number of factors

and actual results may differ, resulting

in future changes to the impairment

allowance. A collective impairment

provision is established for the groups of

homogeneous loans and advances that

are not considered individually significant

and groups of loans that are individually

significant but that were not found to

be individually impaired. A collective

assessment of impairment takes into

account the data from loan portfolio

(such as credit quality, levels of arrears,

credit utilisation, etc.), concentrations

of risk and economic data (including

levels of unemployment, inflation, GDP

growth rate and country rating) and

the performance of different individual

group. The impairment requirements in

SLFRS 9 – “Financial Instruments” are

based on an expected credit loss (ECL)

model and it is reflected the general

pattern of deterioration or improvement,

in the credit quality of financial

instruments. The Group calculates ECLs

either on a collective or an individual

basis. The amount of ECLs recognised as

a loss allowance or provision depends on

the extent of credit deterioration since

initial recognition and measured under

following bases:

• 12-month ECLs (Stage 1), which apply

to all items as long as there is no

significant deterioration in credit risk.

• Lifetime ECLs (Stages 2 and 3), which

apply when a significant increase

in credit risk has occurred on an

individual or collective basis.

Further, the Group makes additional

judgements and estimates with regard to

the following under ECL model.

• The Group’s criteria for assessing if

there has been a significant increase

in credit risk and so impairment for

financial assets should be measured

on a lifetime ECL basis.

• Development of ECL models,

including various formula and the

choice of inputs.

• Determination of association between

macroeconomic inputs, such as

GDP growth, inflation, interest rates,

exchange rates and unemployment

with the effect on probability of

default (PDs), exposure at default

(EAD) and loss given default (LGD).

• Selection of forward-looking

macroeconomic scenarios and their

probability weightings to derive the

economic inputs into the ECL model.

The economic scenarios and forward-

looking macroeconomic assumptions

underpinning the collective provision

calculation are outlined in Note 4.4.11.

As per SLFRS 9 – “Financial Instruments”,

the collective provision for groups of

homogeneous loans is established

using statistical methods or, a formula

approach based on historical loss rate

experience, using the statistical analysis

of historical data on delinquency

to estimate the amount of loss.

Management applies judgement to

ensure that the estimate of loss arrived

at, on the basis of historical information

is appropriately adjusted to reflect the

economic conditions and portfolio factors

as at the reporting date. The loss rates

are regularly reviewed against, actual

loss experience. It has been the Group’s

policy to regularly review its model in

the context of actual loss experience

and adjust when necessary. The accuracy

of the provision depends on the model

assumptions and parameters used in

determining the impairment. Details of

impairment losses on loans and advances

are given in Note 14.

3.3.8.5 Impairment of investment in

subsidiaries, other financial assets

and non-financial assets

The Group and the Bank follow the

guidance of LKAS 36 – “Impairment

of Assets” and SLFRS 9 – “Financial

Instruments” in determining whether

an investment or a financial asset

is impaired. Determination and

identification of impairment indicators

require the Group and the Bank to

evaluate duration and extent to which

the fair value of an investment for a

financial asset is less than its cost and

the financial stability of the near term

business outlook of the investment or the

financial asset, considering the factors

such as performance of the sector and

industry, technology and operational

environmental changes along with future

cash flows. This process involves with

material judgement in aforesaid areas.

3.3.8.6 Defined benefit obligation

The cost of the defined benefit pension

plans and other post- employment

benefit plans are determined using an

actuarial valuation. An actuarial valuation

involves making various assumptions

determining the discount rates, expected

rates of return on planned assets, future

salary increases, mortality rates and future

pension increases. Due to the long-term

nature of these plans, such estimates

are subject to significant uncertainty. In

determining the appropriate discount

rate, the Group considers the interest

rates of Sri Lanka Government Bonds

with maturities corresponding to the

expected duration of the Defined Benefit

Obligation. The mortality rate is based

on publicly available mortality tables.

Future salary increases and pension

increases are based on inflation rate

and salary increase rates of the Group.

All assumptions are reviewed at each

reporting date and assumptions used in

the year are given in Note 48.

3.3.8.7 Fair value of land and

buildings

The freehold land and buildings and

the buildings on leasehold land of

the Group are reflected at fair value

less accumulated depreciation. The

Group engaged independent valuation

specialists to determine fair value of such

properties in terms of the SLFRS 13 –

“Fair Value Measurement”. The details of

valuation of freehold land and buildings

and the buildings on leasehold land are

given in Note 34.

3.3.8.8 Useful life of the property,

plant and equipment and intangible

assets

The Group reviews the residual values,

useful lives and methods of depreciation

of property, plant and equipment and

intangible assets at each reporting

date. Judgement of the Management

is exercised in the estimation of these

values, rates, methods and hence they

are subject to uncertainty. The details

of the depreciation methods and rates

used for each assets category are given

in Note 34.

3.3.8.9 Classification of investment

properties

Management is required to use its

judgement to determine whether a

property qualified as an investment

property. A property that is held to earn

rentals or for capital appreciation or

both and which generates cash flows

largely independently of the other

assets held by the Group are accounted

for as investment properties. On the

other hand, properties that are used for

operations or for the process of providing

services or for administration purposes

and which do not directly generate

cash flows as stand- alone assets are

accounted as property, plant and

equipment.

3.3.8.10 Determination of control

over investees

Subsidiaries are entities that are

controlled by the Bank, control is

achieved when the Bank is exposed,

or has rights to variable returns from

its involvement with the invitee and

has the ability to affect the returns of

those investees through its power over

the investee. The Management applies

its judgements to determine the Bank

controls over its investees.

3.3.8.11 Taxation

The Group is subject to income tax, value

added tax (VAT) and other applicable

taxes. A judgement is required to

determine the total provision for current,

deferred and other taxes due to the

uncertainties that exists with respect

to the interpretation of the applicable

tax laws at the time of preparing these

Financial Statements. The details on

the applicable tax rates and other

information are given under Notes

4.8, 18, and 37. The Group is subject

to transfer pricing regulations and it

is necessitated using management

judgement to determine the impact of

transfer pricing regulations. Accordingly,

critical judgements and estimates were

used in applying the regulations in

aspects including but not limited to

identifying associated undertakings,

estimation of the respective arm’s length

prices and selection of appropriate

pricing mechanism. The current tax

charge is subject to such judgements.

Differences between estimated income

tax charge and actual payable may

arise as a result of variances between

Management’s interpretation and

application of tax regulation.

4

Material accounting

policies

The material accounting policies applied

by the Bank and the Group in preparation

of its Financial Statements are included

below and have been consistently

applied to all periods presented in the

Financial Statements of the Group and

the Bank, unless otherwise indicated.

4.1 Basis of consolidation

The Group’s Financial Statements

comprise consolidation of the Financial

Statements of the Bank and its

Subsidiaries in terms of SLFRS 10 –

“Consolidated Financial Statements”

and LKAS 27 – “Consolidated and

Separate Financial Statements” and the

proportionate share of the profit or loss

and net assets of its Associates in terms

of the Sri Lanka Accounting Standard

LKAS 28 – “Investments in Associates

and Joint Ventures”. The Bank’s Financial

Statements comprise the amalgamation of

the Financial Statements of the Domestic

Banking Unit, the Off-shore Banking Unit

and the Overseas Operations of the Bank.

The detailed accounting policies pertaining

to the consolidation of subsidiaries and

associates are given in the Notes 31 and

32.

4.1.1 Business combinations

The Group determines whether a

transaction or other event is a business

combination by applying the definition

in SLFRS 3 – “Business Combinations”,

which requires that the assets acquired

and liabilities assumed constitute a

business. Business combinations are

accounted for using the acquisition

method. As of the acquisition date, the

amount of non-controlling interest is

measured either at fair value or at the

non-controlling interests’ proportionate

share of the acquirer’s identifiable net

assets. Acquisition related cost are

costs the acquirer incurs to effect a

business combination. Those costs

include finder’s fees, advisory, legal,

accounting, valuation, other professional

consulting fees, general administrative

costs including the cost of maintaining

an Internal Acquisition Department and

cost of registering and issuing debt and

equity securities. Acquisition related

costs, other than those associated with

the issue of debt or equity securities

are expensed in the periods in which

the costs are incurred and the services

are received. The Group elects on a

transaction by transaction basis whether

to measure non-controlling interests

at its fair value or at its proportionate

share of the recognised amount of the

identifiable net assets, at the acquisition

date. Transaction costs, other than those

associated with the issue of debt or

equity securities that the Group incurs in

connection with a business combination

are expensed as incurred.

4.1.2 Loss of control

When the Group loses control over a

subsidiary, it derecognises the assets

and liabilities of the subsidiary, and any

related non-controlling interest (NCI)

and other components of equity. Any

resulting gain or loss is recognised in

profit or loss. Any interest retained in

the former subsidiary is measured at fair

value when control is lost. Further, the

Bank’s share of components previously

recognised in Other Comprehensive

Income (OCI) is reclassified to profit or

loss or retained earnings as appropriate.

Any surplus or deficit arising on the loss

of control is recognised in the profit or

loss. If the Group retains any interest

in the previous subsidiary, then such

interest is measured at fair value at the

date that control is lost. Subsequently, it

is accounted for as an equity-accounted

investee or in accordance with the

Group’s accounting policy for financial

instruments depending on the level of

influence retained.

4.2 Foreign currency translations

4.2.1 Foreign currency transactions

and balances

At the initial recognition, transactions

in foreign currency are translated

into the functional currency of the

operation which is Sri Lankan Rupees

(LKR) at the spot exchange rate at

the date of the transaction. Monetary

assets and liabilities denominated in

foreign currency at the reporting date

are retranslated into the functional

currency at the spot exchange rate at

that date and all differences arising

on non-trading activities are taken to

“Net other operating income” (Note

13) in the Statement of Profit or Loss.

Non-monetary assets and liabilities

that are measured in terms of historical

cost in a foreign currency are translated

using the exchange rate at the date of

the initial recognition. Non-monetary

assets and liabilities denominated in

foreign currency that are measured

at fair value are retranslated into the

functional currency at the spot exchange

rate including any exchange gain or

loss component at the date on which

the fair value is determined. Gain or

loss on a non-monetary item including

exchange component is recognised

in Other Comprehensive Income.

Forward exchange contracts are valued

at the forward market rates ruling on

the reporting date and resulting net

unrealised gains or losses are dealt within

the Statement of Profit or Loss.

4.2.2 Foreign operations

The results and financial position of

foreign operations, whose functional

currencies are not Sri Lankan Rupees,

are translated into Sri Lankan Rupees as

follows:

The assets and liabilities of foreign

operations are translated into Sri Lankan

Rupees at spot exchange rate as at the

reporting date.

The income and expenses of foreign

operations are translated at average

rate for the period. Foreign currency

differences on the translation of foreign

operations are recognised in Other

Comprehensive Income.

When a foreign operation is disposed

off, the relevant amount in the translation

reserve is transferred to the profit or loss

as part of the profit or loss on disposal

in other operating income or other

operating expenses.

4.2.3 Hedge accounting

The Bank enters into hedging

arrangements with the counterparties in

order to mitigate the foreign exchange

risk from foreign currency transactions.

According to the SLFRS 9 - "Financial

Instrument", an entity may designate an

item in its entirety or a component of an

item as the hedged item in a hedging

relationship. A hedging relationship

qualifies for hedge accounting only if

the hedging relationship consists only of

eligible hedging instruments and eligible

hedged items.

At the inception of the hedging

relationship there is formal designation

and documentation of the hedging

relationship and the entity’s risk

management objective and strategy

for undertaking the hedge. That

documentation shall include

identification of the hedging instrument,

the hedged item, the nature of the risk

being hedged and how the entity will

assess whether the hedging relationship

meets the hedge effectiveness

requirements, including its analysis of

the sources of hedge ineffectiveness and

how it determines the hedge ratio.

SLFRS 9 – “Financial Instruments”

enables hedge accounting for three

different designated categories, namely

cash flow hedge (designated for a highly

probable forecasted transaction, a

firm commitment (not recorded on the

balance sheet), foreign currency cash

flows of a recognised asset or liability, or

a forecasted intercompany transaction).

Fair value hedge (designated for a firm

commitment (not recorded) or foreign

currency cash flows of a recognised

asset or liability). Net investment hedge

(designated for the net investment in a

foreign operation). The Bank accounts

the similar transactions, under hedge

accounting treatment specified in the

SLFRS 9 – “Financial Instruments” and

were valued using forward exchange

rates as of each reporting date of such

instruments.

4.3 Classification of financial

instruments between debt and

equity

Classification of financial instruments

between debt and equity depends

on following characteristics of such

instruments:

• Name or labels given to the

instruments

• Presence or absence of a fixed

maturity date

• Life of the instrument

• Source of payments

• Right to enforce payments

• Rights to participate in Management

• Risk involved in the instruments

• Volatility of cash flows

• Securities given as collaterals

4.4 Financial assets and financial

liabilities

4.4.1 Recognition and derecognition

of financial instruments

All financial assets and liabilities are

initially recognised on the settlement

date, i.e. the date that the Group

becomes a party to the contractual

provisions of the instrument. This

includes; “regular way trades”. Regular

way trade means purchases or sales of

financial assets that require delivery of

assets within the time frame generally

established by regulation or convention

in the market place. Loans and

receivables are recognised when cash is

advanced (or settled) to the borrowers.

Financial assets at fair value through

profit or loss are recognised initially at

fair value. All other financial assets are

recognised initially at fair value plus

directly attributable transaction costs.

The Group derecognises a financial asset

when the contractual cash flows from

the asset expire or it transfers its rights

to receive contractual cash flows on the

financial asset in a transaction in which

substantially all the risks and rewards of

ownership are transferred. Any interest in

transferred financial assets that is created

or retained by the Group is recognised as

a separate asset or liability.

A financial liability is derecognised

when the obligation under the liability

is discharged or cancelled or expired.

Where an existing financial liability is

replaced by another from the same

lender on substantially different terms,

or the terms of an existing liability

are substantially modified, such an

exchange or modification is treated as

a derecognition of the original liability

and the recognition of a new liability. The

difference between the carrying value

of the original financial liability and the

consideration paid is recognised in the

Statement of Profit or Loss.

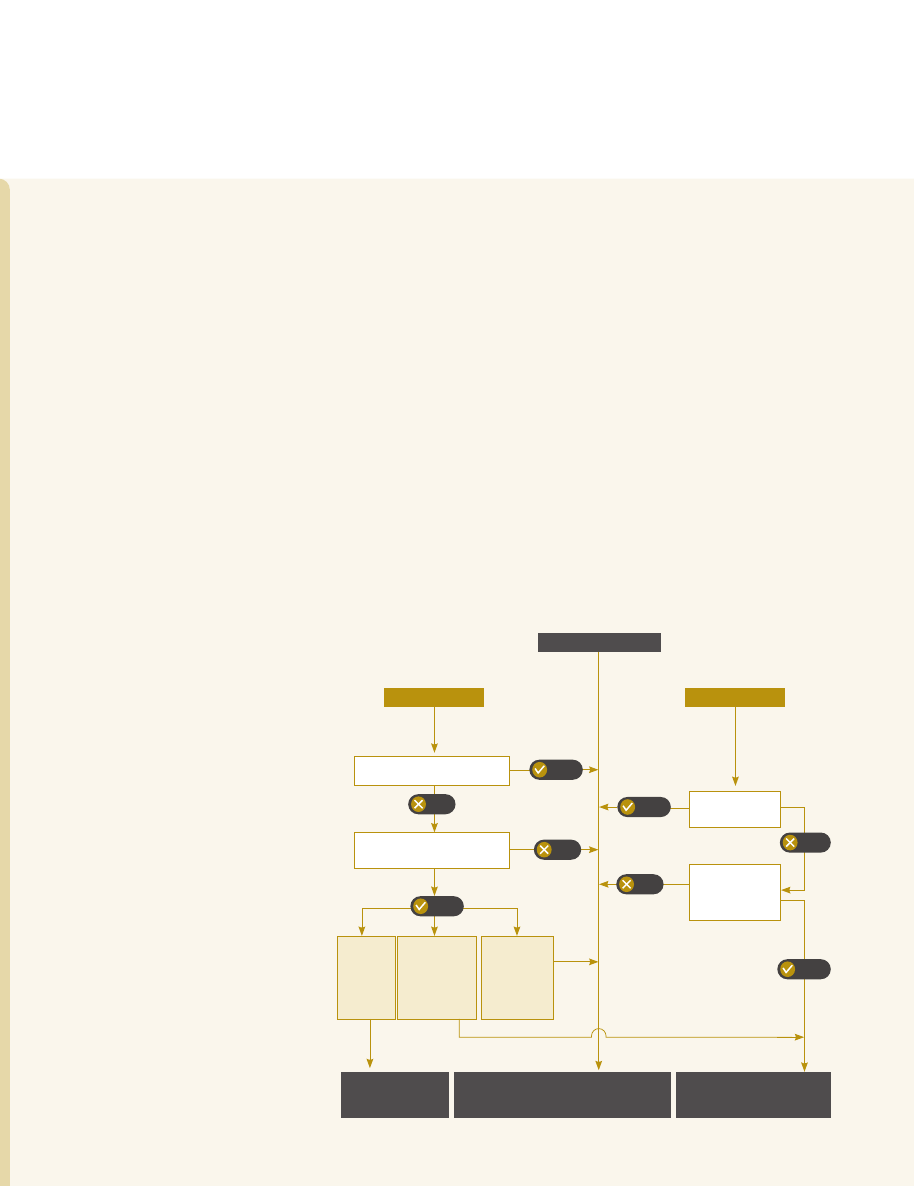

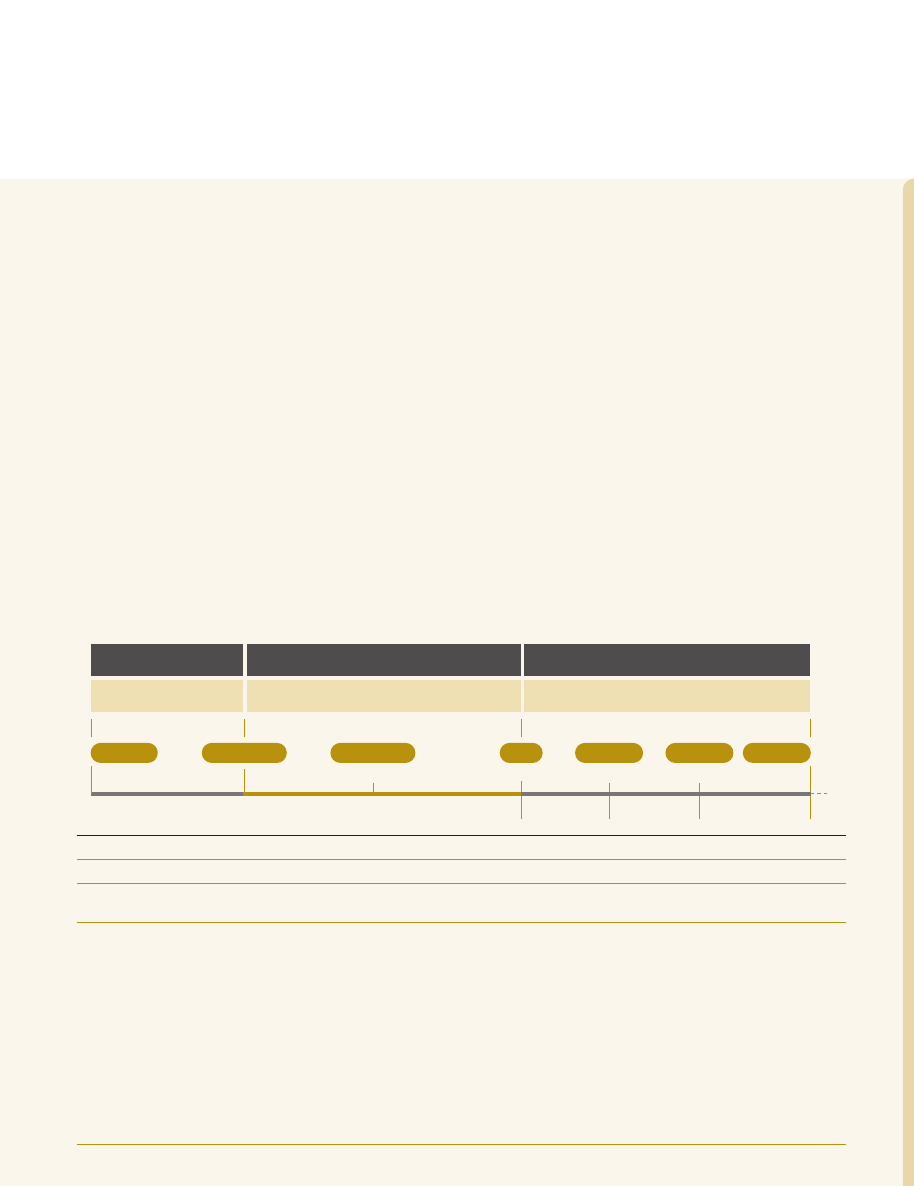

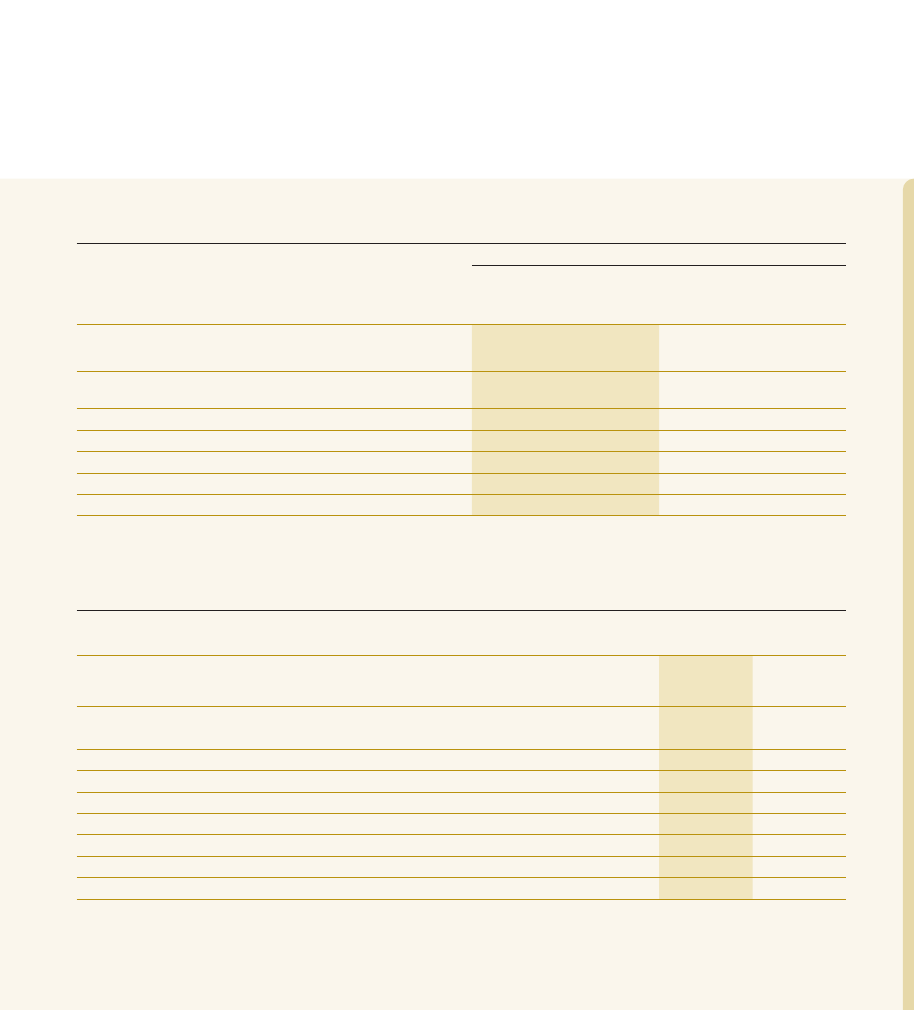

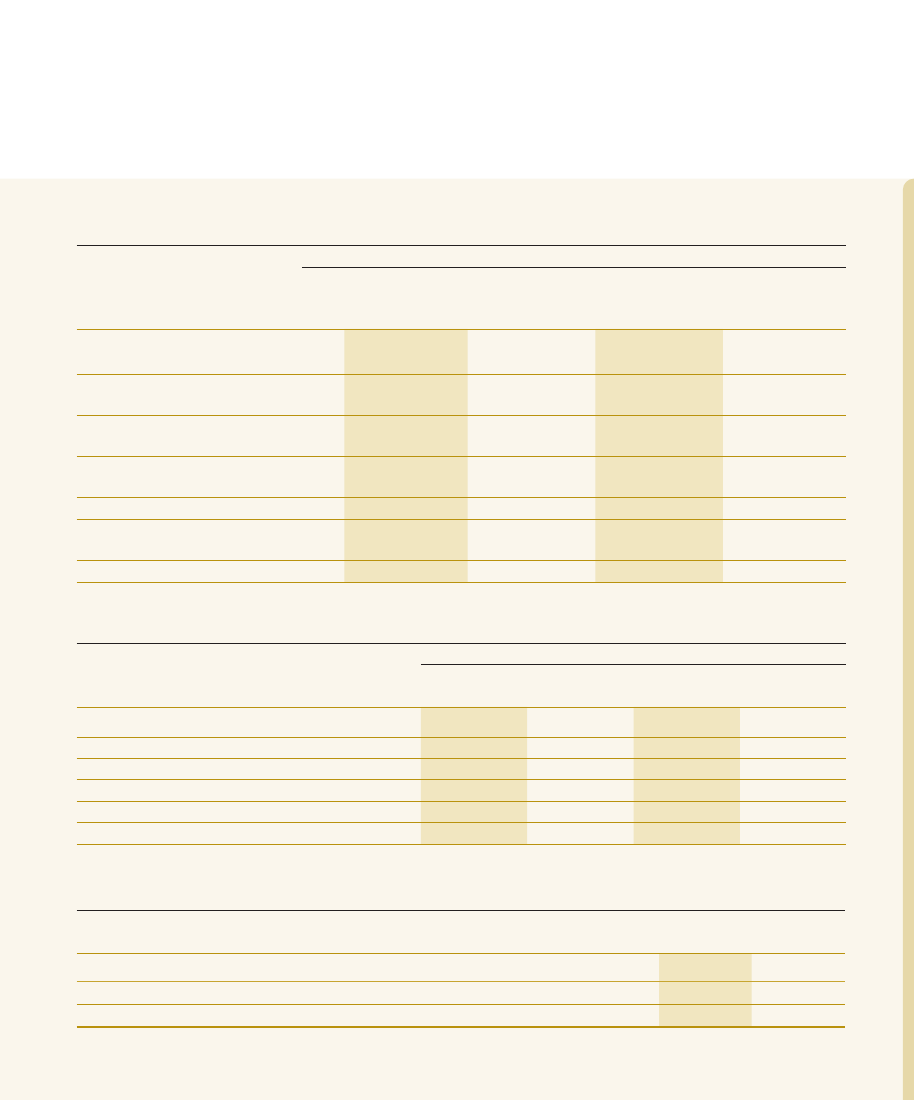

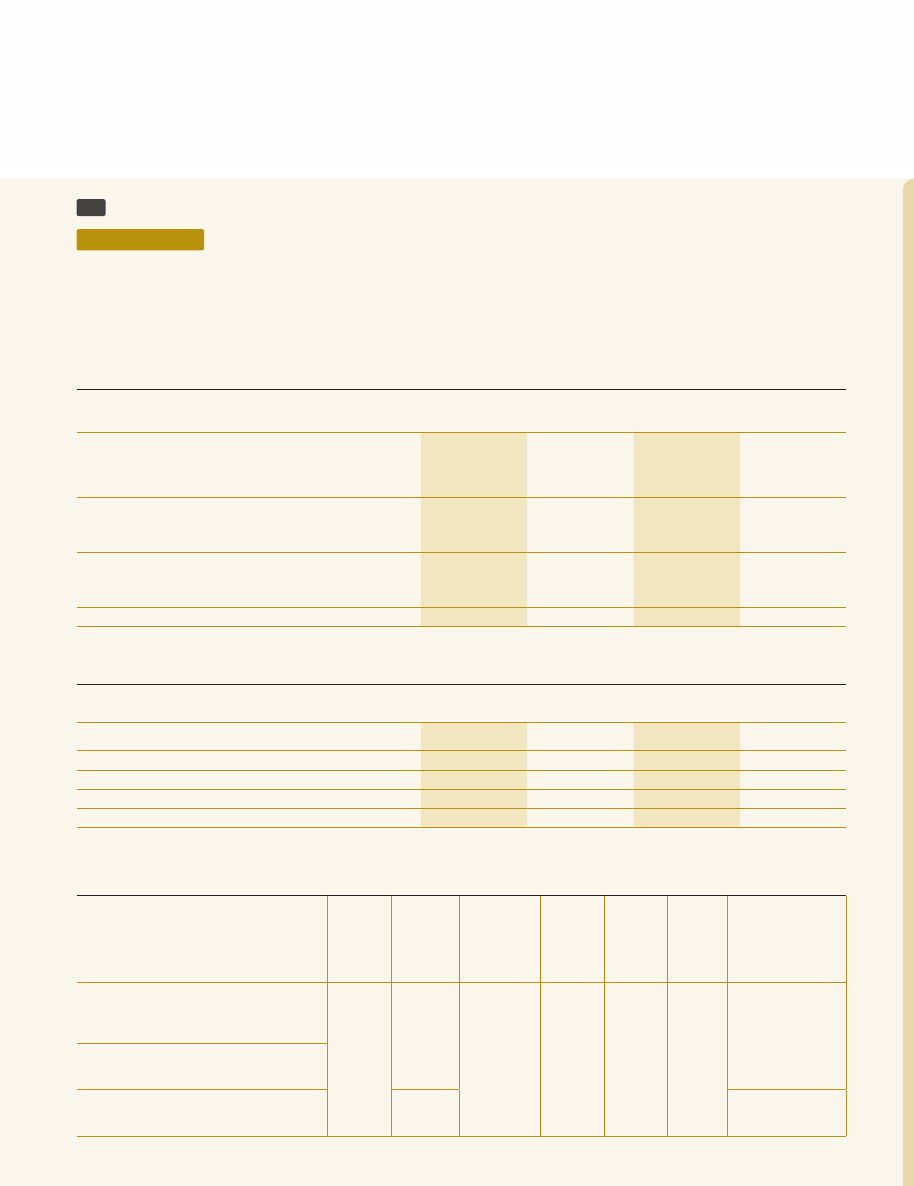

Solely Payments of Principle

and Interest (SPPI)?

Fair value option elected?

Derivative Instrument

Debt Instrument

Held for trading

Elected the

irrecoverable

option of OCI?

Amortised cost

Fair value through other

comprehensive income

Equity instrument

Yes

Yes

Yes

Yes

No

No

No

No

Fair value through profit or loss

Held for

Trading

Held to

collect cash

flows and

for sale

Held to

collect

cash flow

4.4.2 Classification of financial assets and financial liabilities

As per SLFRS 9 – “Financial Instruments”, the classification depends on the Group’s

business model for managing financial assets and the contractual terms of the financial

assets’ cash flows. The following diagram depicts how the Bank classifies the financial

assets.

4.4.2.1 At the inception, the financial

assets are classified in one of the

following categories

• Financial assets measured at fair

value through profit or loss (Notes

4.4.7 and 27)

• Financial assets at amortised cost

– Financial assets at amortised cost

– loans and advances (Note 28)

– Financial assets at amortised

cost - debt and other instruments

(Notes 4.4.8 and 29)

• Financial assets measured at fair

value through other comprehensive

income (Notes 4.4.9 and 30).

4.4.2.2 At the inception, the financial

liabilities are classified in one of the

following categories

• Financial liabilities at amortised cost

– Financial liabilities at amortised

cost – due to depositors (Note 42)

– Financial liabilities at amortised

cost – other borrowings and

subordinated liabilities (Notes 43

and 49)

4.4.3 Initial measurements of financial

instruments

Financial assets and liabilities are

initially measured at their fair value

plus transaction cost, except in the

case of financial assets and liabilities

recorded at fair value through profit

or loss. Transaction cost in relation to

financial assets and liabilities at fair value

through profit or loss are dealt with in the

Statement of Profit or Loss.

4.4.4 “Day One” profit or loss

When the transaction price differs

from the fair value of other observable

current market transactions in the same

instrument or based on a valuation

technique whose variables include only

data from observable markets, the Group

immediately recognises the difference

between the transaction price and fair

value (a “Day One” profit or loss) in the

Statement of Profit or Loss. In cases

where fair value is determined using data

which is not observable, the difference

between the transaction price and model

value is only recognised in the Statement

of Profit or Loss over the life of the

instrument.

4.4.5 Business model assessment

With effect from 1 January 2018, as per

SLFRS 9 – “Financial Instrument”, the

Group classifies all of its financial assets

based on the business model and makes

an assessment of the objective of a

business model in which an asset is held

at a portfolio level and not assessed on

instrument by – instrument basis because

this best reflects the way the business is

managed and information is provided

to management. The information

considered includes:

• The stated policies and objectives

for the portfolio and the operation

of those policies in practice. In

particular, whether Management’s

strategy focuses on earning

contractual interest revenue,

maintaining a particular interest rate

profile, matching the duration of the

financial assets to the duration of

the liabilities that are funding those

assets or realising cash flows through

the sale of the assets;

• How the performance of the portfolio

is evaluated and reported to the

Bank’s management;

• The risks that affect the performance

of the business model (and the

financial assets held within that

business model) and how those risks

are managed;

• How managers of the business

are compensated – e.g. whether

compensation is based on the fair

value of the assets managed or the

contractual cash flows collected; and

• The frequency, volume and timing

of sales in prior periods, the reasons

for such sales and its expectations

about future sales activity. However,

information about sales activity is not

considered in isolation, but as part

of an overall assessment of how the

Bank’s stated objective for managing

the financial assets is achieved and

how cash flows are realised.

The business model assessment is

based on reasonably expected scenarios

without taking “worst case” or “stress

case” scenarios into account. If cash

flows after initial recognition are realised

in a way that is different from the Bank’s

original expectations, the Bank does not

change the classification of the remaining

financial assets held in that business

model, but incorporates such information

when assessing newly originated or newly

purchased financial assets going forward.

4.4.6 Assessment of whether

contractual cash flow characteristics

are met the Solely Payments of Prin-

cipal and Interest (SPPI test)

As a second step of assets classification

process, the Group assesses the

contractual terms of financial assets to

identify whether they meet the SPPI test.

For the purposes of this assessment,

“principal” is defined as the fair value of

the financial asset on initial recognition

and may change over the life of the

financial asset (for example, if there are

repayments of principal or amortisation

of the premium/discount).

“Interest” is defined as consideration

for the time value of money and for the

credit risk associated with the principal

amount outstanding during a particular

period of time and for other basic

lending risks and costs, as well as profit

margin.

In contrast, contractual terms that

introduce a more than de minimise

exposure to risks or volatility in the

contractual cash flows that are unrelated

to a basic lending arrangement do

not give rise to contractual cash flows

that are solely payments of principal

and interest on the principal amount

outstanding. In such cases, the financial

asset is required to be measured at fair

value through profit and loss.

In assessing whether the contractual cash

flows are solely payments of principal

and interest on principal amount

outstanding, the Group considers the

contractual terms of the instrument. This

includes assessing whether the financial

asset contains a contractual term that

could change the timing or amount of

contractual cash flows such that it would

not meet this condition. In making the

assessment, the Group considers:

• Contingent events that would change

the amount and timing of cash flows

• Leverage features;

• Prepayment and extension terms;

• Terms that limit the Group’s claim to

cash flows from specified assets; and

• Features that modify consideration of

the time value of money

4.4.7 Financial assets measured at

fair value through profit or loss

Items at fair value through profit or loss

comprise:

• Items held for trading purpose;

• Items specifically designated as fair

value through profit or loss on initial

recognition; and

• Debt instruments with contractual

terms that do not represent solely

payments of principal and interest.

Financial instruments held at fair

value through profit or loss are initially

recognised at fair value, with transaction

costs recognised in the Statement of

Profit or Loss as incurred. Subsequently,

they are measured at fair value and any

gains or losses are recognised in the

Statement of Profit or Loss as they arise.

Where a financial asset is measured at

fair value, a credit valuation adjustment is

included to reflect the credit worthiness

of the counterparty, representing the

movement in fair value attributable to

changes in credit risk.

4.4.7.1 Financial instruments held for

trading purpose

A financial instrument is classified as

held for trading if it is acquired or

incurred principally for the purpose of

selling or repurchasing in the near term,

or forms part of a portfolio of financial

instruments that are managed together

and for which there is evidence of short-

term profit taking, or it is a derivative

not in a qualifying hedge relationship.

Trading derivatives and trading securities

are classified as held for trading and

recognised at fair value in the Statement

of Financial Position. Changes in fair

value are recognised in “Net gains/

(losses) from trading” (Note 10) and “Net

fair value gains/(losses) from financial

instruments at fair value through profit

or loss” (Note 11). Interest income from

financial instruments held for trading is

recorded under “Net interest income”

(Note 8) while dividend income is

recorded in “Net gains/(losses) from

trading” (Note 10) when the right to

payment has been established.

4.4.7.2 Financial instruments

designated and measured at fair

value through profit or loss

Upon initial recognition, financial

instruments may be designated and

measured at fair value through profit

or loss. A financial asset may only be

designated at fair value through profit or

loss if doing so eliminates or significantly

reduces measurement or recognition

inconsistencies (i.e. eliminates an

accounting mismatch) that would

otherwise arise from measuring financial

assets or liabilities on a different basis.

A financial liability may be designated

at fair value through profit or loss if it

eliminates or significantly reduces an

accounting mismatch or:

• If a host contract contains one or

more embedded derivatives; or

• If financial assets and liabilities are

both managed and their performance

evaluated on a fair value basis in

accordance with a documented

risk management or investment

strategy. Where a financial liability is

designated at fair value through profit

or loss, the movement in fair value

attributable to changes in the Group’s

own credit quality is calculated by

determining the changes in credit

spreads above observable market

interest rates and is presented

separately in other comprehensive

income. As of 31 December 2023,

there were no any financial liability

designated at fair value through profit

or loss.

4.4.7.3 Debt instruments with

contractual terms that do not

represent the solely payments of

principal and interest

Financial debt instruments which are not

meet solely payments of principal and

interest test will be classified as fair value

through profit or loss.

4.4.8 Financial assets measured at

amortised cost-debt instruments

Investments in debt instruments are

measured at amortised cost where they

have:

• Contractual terms that give rise to

cash flows on specified dates, that

represent solely payments of principal

and interest on the principal amount

outstanding; and

• Are held within a business model

whose objective is achieved by

holding to collect contractual cash

flows.

These debt instruments are initially

recognised at fair value plus directly

attributable transaction costs and

subsequently measured at amortised

cost using effective interest rate (EIR).

The measurement of credit impairment is

based on the three stage expected credit

loss model described below in Note

4.4.11 Impairment of financial assets.

4.4.9 Financial assets measured at fair

value through other comprehensive

income

4.4.9.1 Debt instruments

Investments in debt instruments are

measured at fair value through other

comprehensive income where they have:

• Contractual terms that give rise to

cash flows on specified dates, that

represent solely payments of principal

and interest on the principal amount

outstanding; and

• Are held within a business model

whose objective is achieved by both

collecting contractual cash flows and

selling financial assets.

These debt instruments are initially

recognised at fair value plus directly

attributable transaction costs and

subsequently measured at fair value.

Gains and losses arising from changes

in fair value are included in Other

Comprehensive Income within a separate

component of equity. Impairment losses

or reversals, interest revenue and foreign

exchange gains and losses are recognised

in profit or loss. Upon disposal, the

cumulative gain or loss previously

recognised in other comprehensive

income is reclassified from other

comprehensive income to profit or loss.

The measurement of credit impairment is

based on the three stage expected credit

loss model as applied to financial assets at

amortised cost. The expected credit loss

model is described below in Note 4.4.11

Impairment of financial assets.

4.4.9.2 Equity instruments

Investment in equity instruments that are

neither held for trading nor contingent

consideration recognised by the Group in

a business combination to which SLFRS

3 – “Business Combinations” applies,

are measured at fair value through

other comprehensive income, where

an irrevocable election has been made

by management. For portfolios where

management does not consider an

irrevocable election of adopting fair value

through other comprehensive income, by

default such investments shall be measured

at fair value through profit or loss.

Upon derecognition, the cumulative

gain or loss recognised in Other

Comprehensive Income are not

transferred to profit or loss. However,

cumulative gain or loss recognised full

derecognition will be transferred from

Other Comprehensive Income reserve

to retained earnings within the equity.

Dividends on such investments are

recognised in “Net other operating

income” (Note 13) in the profit or loss.

4.4.10 Reclassification of financial

assets

The Group reclassifies its financial

assets when, and only when, the Group

changes its business model for managing

financial assets. If the Group reclassifies

financial assets which were measured at

amortised cost, fair value through other

comprehensive income or fair value

through profit or loss, the Group applies

the reclassification prospectively from the

reclassification date. The Group does not

restate any previously recognised gains,

losses (including impairment losses) or

interest.

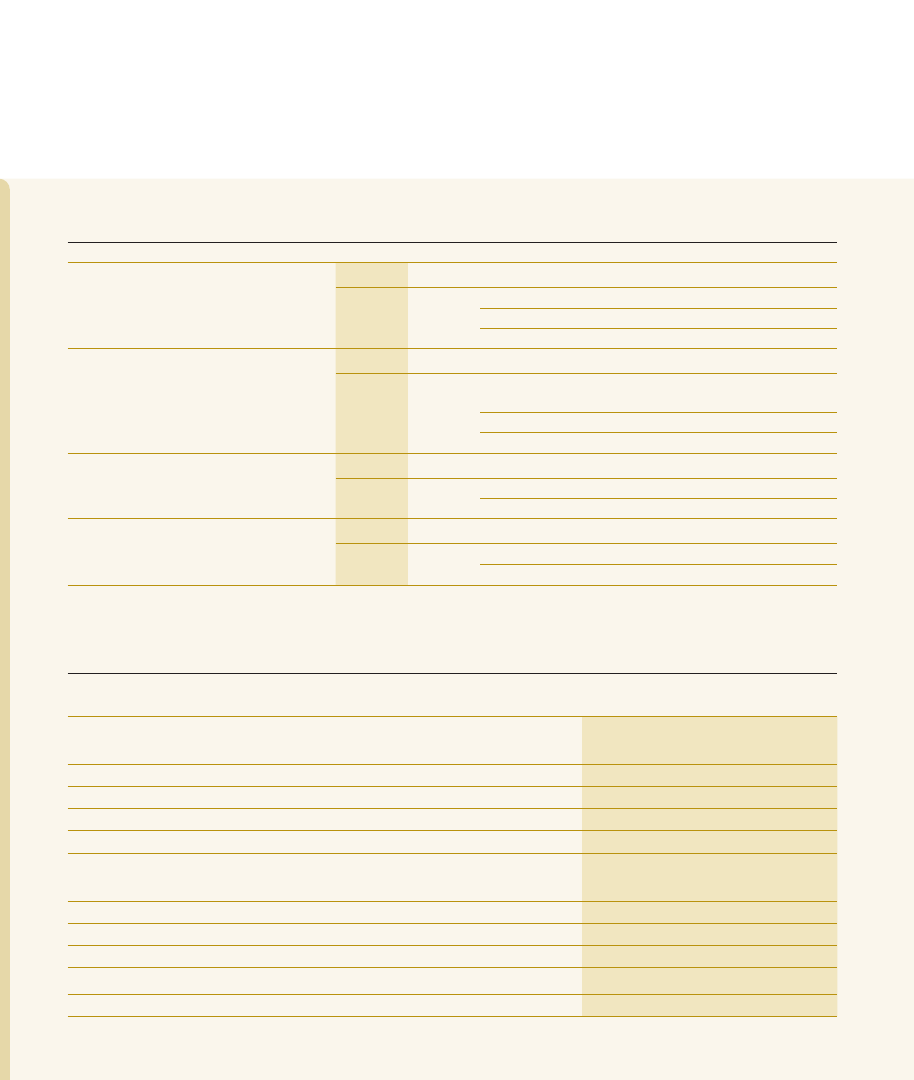

Initial Measurement

Measurement after

reclassification

Treatment on reclassification

Fair value through profit

or loss

Amortised cost

Fair value at the reclassification date becomes its new gross carrying amount. The

effective interest rate is calculated on the basis of that amount. For the purpose of

applying the impairment requirements, the reclassification date is treated as the date

of initial application.

Fair value through profit

or loss

Fair value through other

comprehensive income

The fair value of the financial asset at the reclassification date becomes its new

carrying amount and the effective interest rate is determined on the basis of the fair

value of the asset at the reclassification date.

Fair value through other

comprehensive

Amortised cost

The cumulative gain or loss previously recognised in Other Comprehensive Income is

removed from equity and adjusted against the fair value of the financial asset at the

reclassification date. The effective interest rate and the measurement of expected

credit losses are not adjusted as a result of the reclassification.

Fair value through other

comprehensive income

Fair value through profit

or loss

The fair value of the financial asset at the reclassification date becomes its new

carrying amount. The cumulative gain or loss previously recognised in Other

Comprehensive Income is reclassified from equity to profit or loss as a reclassification

adjustment at the reclassification date.

Amortised cost

Fair value through profit

or loss

Any gain or loss arising from a difference between the previous amortised cost of the

financial asset and fair value at the reclassification date is recognised in profit or loss.

Amortised cost

Fair value through other

comprehensive income

Any gain or loss arising from a difference between the previous amortised cost

of the financial asset and fair value at the reclassification date is recognised in

Other Comprehensive Income. The effective interest rate and the measurement of

expected credit losses are not adjusted as a result of the reclassification.

The table below summaries the treatment of gains and losses on reclassification:

4.4.10.1 Upgrading of financial

instruments

According to the CBSL Direction No.

14 of 2021, the Bank can upgrade

Financial Instruments from a higher stage

in accordance with a policy approved

by the Board of Directors. Therefore,

the Bank will upgrade the Financial

Instruments to a higher stage with the

consent of the Chief Risk Officer with the

proper rational for such upgrade.

4.4.11 Impairment of financial assets

The Group applies a three-stage

approach in measuring expected credit

loss (ECL) for the following categories of

financial assets that are not measured at

fair value through profit or loss:

• Debt instruments measured at

amortised cost and fair value through

other comprehensive income;

• Loan commitments and

Financial guarantee contracts.

No ECL is recognised on equity

investments.

The Group performs an assessment at

the end of each reporting period, of

whether a financial instrument’s credit

risk has increased significantly since initial

recognition, by considering the change

in the risk of default occurring over the

remaining life of the financial instrument.

Based on this process financial assets

migrate through the following three

stages based on the change in credit risk

since initial recognition.

4.4.11.1 Stage 1: 12 months ECL

For exposures where there has not

been a significant increase in credit risk

since initial recognition and that are not

credit impaired upon origination, the

portion of the lifetime ECL associated

with the probability of default events

occurring within the next 12 months is

recognised. The Bank determines 12

months ECL from customers whom are

not significantly credit deteriorated.

4.4.11.2 Stage 2: Lifetime ECL

For exposures where there has been a

significant increase in credit risk since

initial recognition but are not credit

impaired, a lifetime ECL (i.e. reflecting

the remaining lifetime of the financial

asset) is recognised.

4.4.11.3 Stage 3: Lifetime ECL

Exposures are assessed as credit

impaired when one or more events

that have a detrimental impact on the

estimated future cash flows of that asset

have occurred. For exposures that have

become credit impaired, a lifetime ECL

is recognised and interest revenue is

calculated by applying the effective

interest rate to the amortised cost (net of

provision) rather than the gross carrying

amount.

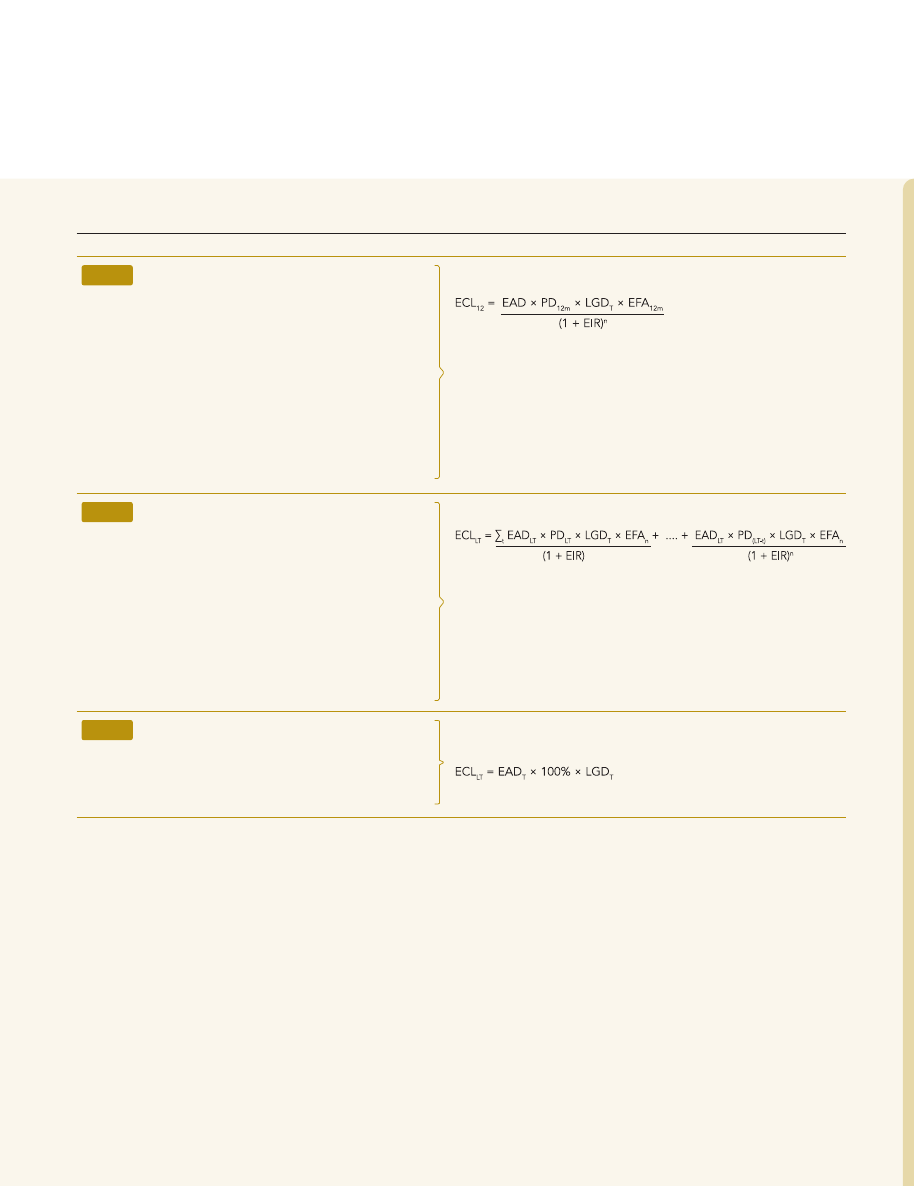

4.4.11.4 Calculation of ECL

The Group calculates ECL based on a

three probability weighted scenarios to

measure the expected cash shortfalls,

discounted at an approximation to

the effective interest rate (EIR). A cash

shortfall is the difference between the

cash flows that are due to an entity

in accordance with the contract and

the cash flows that the entity expects

to receive. The mechanics of the ECL

calculations of the Group are outlined

below and the key elements are, as

follows:

Probability of default (PD)

PD is an estimate of the likelihood of

default over a given time horizon. A

default may only happen at a certain time

over the assessed period, if the facility

has not been previously recognised and

is still in the portfolio. The concept of

PDs is further explained in Note 28.

Exposure at default (EAD)

EAD is an estimate of the exposure at a

future default date, taking into account

expected changes in the exposure after

the reporting date, including repayments

of principal and interest, whether

scheduled by contract or otherwise,

expected drawdowns on committed

facilities, and accrued interest from

missed payments. The EAD is further

explained in Note 28.

Loss given default (LGD)

LGD is an estimate of the loss arising

in the case where a default occurs at a

given time. It is based on the difference

between the contractual cash flows due

and those that the lender would expect

to receive, including from the realisation

of any collateral. It is usually expressed

as a percentage of the EAD. The LGD is

further explained in Note 28.

4.4.11.5 Determining the stage for

impairment

At each reporting date, the Group

assesses whether there has been a

significant increase in credit risk for

exposures since initial recognition by

comparing the risk of default occurring

over the expected life between the

reporting date and the date of initial

recognition. The Group considers

reasonable and supportable information

that is relevant and available without

undue cost or effort for this purpose.

This includes quantitative and qualitative

information and also, forward-looking

analysis.

An exposure will migrate through the

ECL stages as asset quality deteriorates.

If, in a subsequent period, asset

quality improves and also reverses any

previously assessed significant increase

in credit risk since origination, then the

provision for doubtful debts reverts

from lifetime ECL to 12 months ECL.

Exposures that have not deteriorated

significantly since origination, or where

the deterioration remains within the

Group’s investment grade criteria, or

which are less than 30 days past due, are

considered to have a low credit risk. The

impairment provision for these financial

assets is based on a 12 months ECL.

The Group assesses whether the credit

risk on an exposure has increased

significantly on an individual or collective

basis. For the purposes of a collective

evaluation of impairment, financial

instruments are grouped on the basis of

shared credit risk characteristics, taking

into account of instrument type, credit

risk ratings, collateral type, date of initial

recognition, remaining term to maturity,

industry, geographical location of the

borrower and other relevant factors.

4.4.11.6 Impairment calculation for

loans and advances

The Bank uses rebuttable presumption

in calculating the impairment for loans

and advances which is permitted under

SLFRS 9 – “Financial Instruments”. The

loan portfolio is classified into three

stages based on the past due days as

follows and the level of applicability

STAGE

Performing

Under performing

Non-performing

STAGE

Origination

30 Days DPD

60 Days DPD

180 Days

270 Days

360 Days

NPCF

(more than 90 days)

Special mention

Substandard

Doubtful

Loss

STAGE

1

3

2

of 12 months ECL and lifetime ECL

depends on the stages. The value and

type of security obtained against the

credit facilities are not considered when

determining the classification status

of a credit facility. In cases where a

borrower has several current accounts

with overdraft limits with the Bank, the

aggregate sanctioned limit and the daily

outstanding aggregate balance on all

such accounts shall be considered for the

purposes of classification of overdrafts.

4.4.11.6.1 Performing credit facilities

(a) All the credit facilities classified as

Stage 1 under SLFRS 9 – “Financial

Instruments” and

(b) All credit facilities identified as

significant increase in credit risk

facilities and classified as Stage

2 under SLFRS 9 – “Financial

Instruments” (Under-performing

credit facilities)

4.4.11.6.2 Non-performing credit

facilities (NPCF)

Non-performing credit facilities (NPCF)

shall mean all credit facilities where;

(a) Contractual payments of a customer

are past due for more than 90 days

(the number of days past due shall

be calculated starting from the

contractual due date of the payment).

(b) Sanctioned limit has remained in

excess for more than 90 days.

(c) Any other credit facilities classified as

Stage 3 as per SLFRS 9 – “Financial

Instruments” (facilities classified as

NPCF based on potential risk and

impaired assets at origination).

Performing

Non-performing credit facilities (NPCF)

Stage 01

Stage 02

Stage 03

• 30 days or less than 30 days

past due

• 31 to 89 days past due

• 90 days or more than 90 days past due

• All credit facilities, which are

not categorised under Stages

2 or 3

• All restructured loans, which are

restructured up to two times, other than

credit facilities upgraded and under

the satisfactory performing period of a

minimum 90 days from the due date of

the 1st capital and/ or interest instalment

post-restructure.

• Under-performing credit facilities/

exposures as significant credit

deterioration identified based on the

deterioration factors given under the

Note 28 – “Financial assets at amortised

cost - Loans and advances”.

• All restructured loans, which are restructured more than

twice, other than credit facilities/exposures upgraded

and under the satisfactory performing period of a

minimum 90 days from the due date of the 1st capital

and/or interest installment post-restructure.

• All rescheduled loans, other than credit

facilities/exposures.

• All credit facilities/customers classified as

non-performing as per CBSL Directions.

• Customers identified with significant credit

deterioration as per the deterioration factors given

under Note 28 – “Financial assets at amortised

cost - Loans and advances”.

For the above classification purpose, facility is considered as restructured facility if original repayment terms have been amended

due to deterioration in credit quality and “Credit Forbearance Policy” of the Bank should be referred in identifying the restructured

facilities. As per the Credit Forbearance Policy of the Bank, following changes/criteria are recognised as changes to the original

repayment terms of a credit facility

• Change of Interest Rate

• Change of Tenor (Maturity)

• Changes to the Grace Period

• Interest Waivers

4.4.11.6.3 Subcategorisation of non-performing credit facilities (NPCF)

NPCF are further categorised into four categories based on the past due days and level of potential risk identified as follows:

Category

Past due days

Potential risk criteria

Special mention

> 90 and < = 180

Exhibits potential weaknesses where, if not corrected in a timely manner,

may adversely affect repayment ability of the customer in future.

Substandard

> 180 and < = 270

Exhibits definable weaknesses, either in respect of the business, cash flow

or financial position of the customer that may jeopardize repayment on

existing terms and uncertainty on the repayment.

Doubtful

> 270 and > = 360 days

Exhibit a high risk or partial default or where full collection is improbable

and there is a high risk of default.

Loss

> 360 days

Deemed to be uncollectable or are almost certain repayment will not be

done and all other NPCF which are not included under above categories.

NOTES TO THE FINANCIAL STATEMENTS

4.4.11.7 Upgrading of credit facilities

Upgrading of credit facilities among the

stages will be done based on the level

of improvement in credit deterioration at

the later assessment dates comparing to

the initial point.

The Bank will upgrade the credit facilities

in accordance with the guidelines

provided under the Credit Risk

Management Policy pertaining to the

upgrading of credit facilities.

4.5 Impairment of non-financial

assets

The Group assesses at each reporting

date whether there is an indication

that an asset may be impaired. If

any indication exists, or when annual

impairment testing for an asset is

required, the Bank estimates the

asset’s recoverable amount. An asset’s

recoverable amount is the higher of an

asset’s fair value less costs to sell or its

value in use. Where the carrying amount

of an asset exceeds its recoverable

amount, the asset is considered impaired

and is written down to its recoverable

amount. In assessing the value in use,

the estimated future cash flows are

discounted to their present value using a

pre-tax discount rate that reflects current

market assessments of the time value of

money and the risks specific to the asset.

In determining fair value less costs to sell,

an appropriate valuation model is used.

These calculations are corroborated by

valuation multiples, quoted share prices

for publicly-traded subsidiaries or other

valuable fair value indicators.

4.6 Fiduciary services

The Group provides fiduciary services

to third parties that result in holding of

the assets on behalf of its customers.

Assets held in fiduciary capacity are not

recognised in the Financial Statements,

as the Group is not the beneficial owner

or does not control such assets.

4.7 Provisions

A provision is recognised as a result

of a past event, when the Group has a

present (legal or constructive) obligation

that can be estimated reliably and it is

probable that an outflow of economic

benefits will be required to settle the

obligation. The amount recognised is

the best estimate of the consideration

required to settle the present obligation

at the reporting date, taking into

account the risks and uncertainties

surrounding the obligation at that date.

Where a provision is measured using

the cash flows estimated to settle the

present obligation, its carrying amount

is determined based on the present

value of those cash flows. A provision for

onerous contracts is recognised when

the expected benefits to be derived

by the Group from a contract are lower

than the unavoidable cost of meeting

its obligations under the contract. The

provision is measured as the present

value of the lower of the expected cost

of terminating the contract and the

expected net cost of continuing with the

contract.

4.8 Income tax expense and other

taxes

4.8.1 Income tax expense

Income tax expense comprises current

and deferred tax. More details are given

in Note 18.

4.8.2 Value added tax (VAT) on

financial services

The base for value added tax

computation is arrived by aggregating

the accounting profit before income tax

and emoluments of employees which is

adjusted for the depreciation computed

on prescribed rates. During the year,

the Group’s total value addition was

subjected to 18% with effect from 1

January 2022 as per the Value Added Tax

Act, No. 14 of 2002 and amendments

thereto. Also the Group is following value

attributable method to compute VAT on

financial services.

4.8.3 Crop insurance levy (CIL)

As per the provisions of the Finance Act,

No. 12 of 2013, the CIL was introduced

with effect from 1 April 2013 and is

payable 1% of the profit after tax to the

National Insurance Trust Fund Board.

4.8.4 Social security contribution levy

(SSCL)

In terms of the Social Security Contribution

Levy Act, No. 25 of 2022, the Bank is

liable for Social Security Contribution

Levy on financial services with effect from

1 October 2022 on the value addition

attributable to financial services at the rate

of 2.5%. Further, SSCL on non-financial

services are made liable on the turnover at

the rate of 2.5%.

4.8.5 Withholding tax (WHT) on

dividends distributed by the Bank,

Subsidiaries and Associates

Withholding tax on dividends distributed

by the Bank

The Bank distributes dividend to its

sole shareholder, the Government of

Sri Lanka. As per the third schedule of

Inland Revenue Act, No 24 of 2017 and

amendments thereto, amounts derived

by the Government of Sri Lanka is

exempted from income tax. Accordingly,

no withholding tax is deducted on

dividend payments made to the

Government of Sri Lanka.

WHT on dividends distributed by the

subsidiaries and associates

As per the Inland Revenue (Amendment)

Act, No. 45 of 2022 WHT on dividends

has been introduced with effect from

1 January 2023. Accordingly, dividend

income received from subsidiaries and

associate companies is liable for WHT at

the rate of 15% and it is a final tax for the

Bank.

5

Insurance business

5.1 Reinsurance

The Group cedes insurance risk in

the normal course of business for all

of its businesses. Reinsurance assets

represent balances due from reinsurance

companies. Amounts recoverable from

reinsurers are estimated in a manner

consistent with the outstanding claims

provision or settled claims associated

with the reinsurer’s policies and are in

accordance with the related reinsurance

contract. Reinsurance assets are reviewed

for impairment at each reporting date or

more frequently when an indication of

impairment arises during the reporting

year. Impairment occurs when there is

objective evidence as a result of an event

that occurred after initial recognition

of the reinsurance asset that the Group

may not receive all outstanding amounts

due under the terms of the contract

and the event has a reliably measurable

impact on the amounts that the Group

will receive from the reinsurer. The

impairment loss is recorded in the

Statement of Profit or Loss. Premiums

and claims are presented on a gross

basis for reinsurance. Reinsurance assets

or liabilities are derecognised when the

contractual rights are extinguished or

expire or when the contract is transferred

to another party.

5.2 Insurance receivables

Insurance receivables are recognised

when due and measured on initial

recognition at the fair value of the

consideration receivable. The carrying

value of insurance receivables is reviewed

for impairment whenever events or

circumstances indicate that the carrying

amount may not be recoverable, with

the impairment loss recorded in the

Statement of Profit or Loss.

5.3 Deferred expenses

5.3.1 Deferred acquisition costs

(DAC)

The costs of acquiring new businesses

including commission, underwriting,

marketing and policy issue expenses

which vary with and directly related to

production of new businesses and/or

investment contracts with discretionary

participation features (DPF), are deferred

to the extent that these costs are

recoverable out of future premiums. All

other acquisition costs are recognised as

an expense when incurred. Subsequent

to initial recognition, DAC for general

insurance is amortised over the period

on the basis unearned premium is

amortised. The reinsurances’ share of

deferred acquisition cost is amortised

in the same manner as the underlying

assets amortisation is recorded in the

Statement of Profit or Loss. Changes in

the expected useful life or the expected

pattern of consumption of future

economic benefits embodied in the

assets are accounted for by changing

the amortisation period and are treated

as a change in an accounting estimate.

DAC are derecognised when the related

contracts are either expired or cancelled.

5.4 Reinsurance commissions

Commissions receivable on outwards

reinsurance contracts are deferred and

amortised over the period of reinsurance.

5.5 Investment contract liabilities

Investment contracts are classified

between contracts with and without

DPF. The accounting policies for

investment contract liabilities with DPF

are the same as those for life insurance

contract liabilities. Investment contract

liabilities without DPF are recognised

when contracts are entered into and

premiums are charged. These liabilities

are initially recognised at fair value being

the transaction price excluding any

transaction costs directly attributable to

the issue of the contract. Subsequent to

initial recognition, investment contract

liabilities are measured at fair value

through profit or loss. Deposits and

withdrawals are recorded directly as

an adjustment to the liability in the

Statement of Financial Position. Fair

value adjustments are performed at

each reporting date and are recognised

in the Statement of Profit or Loss. Fair

value is determined through the use

of prospective discounted cash flow

techniques. For unitised contracts, fair