The Bank supported by its effective risk management framework successfully achieved its highest ever profit in 2023 amidst significant challenges posed by the subdued global economic outlook, geopolitical fragmentation and spillover effects of adverse economic conditions. Debt restructuring, results of the Bank diagnostic exercise and forward looking loan loss provisions have been identified as the areas with potential ramifications.

Dwindling disposable income resultant from high rate of inflation and fiscal consolidation measures continued to impact the debt servicing capacity of the borrowers. As a result of monetary policy easing measures adopted and inflation reaching a single digit since mid 2023 it is expected to ease off the pressure on the balance sheet.

Throughout the year, Bank continued its efforts to refrain from transferring the increasing interest rate impact especially to the existing borrowers in the retail segment. Due to the unprecedented monetary tightening prevailed during the first half, year-on-year contraction in the loan book was observed. However, with the monetary easing since mid 2023 year closed on a growth trajectory.

Gradual normalisation of interest rates of Government securities was observed in the aftermath of the domestic debt optimisation, paving the way to effective transmission of monetary policy. During the second half of 2023 a reduction in the market interest rates was observed in line with the downward adjustment of policy interest rates.

Significant improvement in Bank’s liquidity position was observed in line with market liquidity as a result of reduction of Statutory Reserve Ratio (SRR), CBSL forex absorptions from the market and targeted measures to curtail overreliance on standing facilities.

Despite numerous challenges such as Domestic Debt Optimisation (DDO) and restructuring of State-Owned Enterprises (SOEs), the Bank as the largest contributor to the country’s financial sector, successfully maintained Capital Adequacy and other regulatory ratios well above the limit.

Subsequent segments will explore the importance of the Bank of Ceylon's Risk Management function in navigating through a demanding regulatory, operational landscape while maintaining the Bank's commitment in facilitating inclusive and sustainable growth.

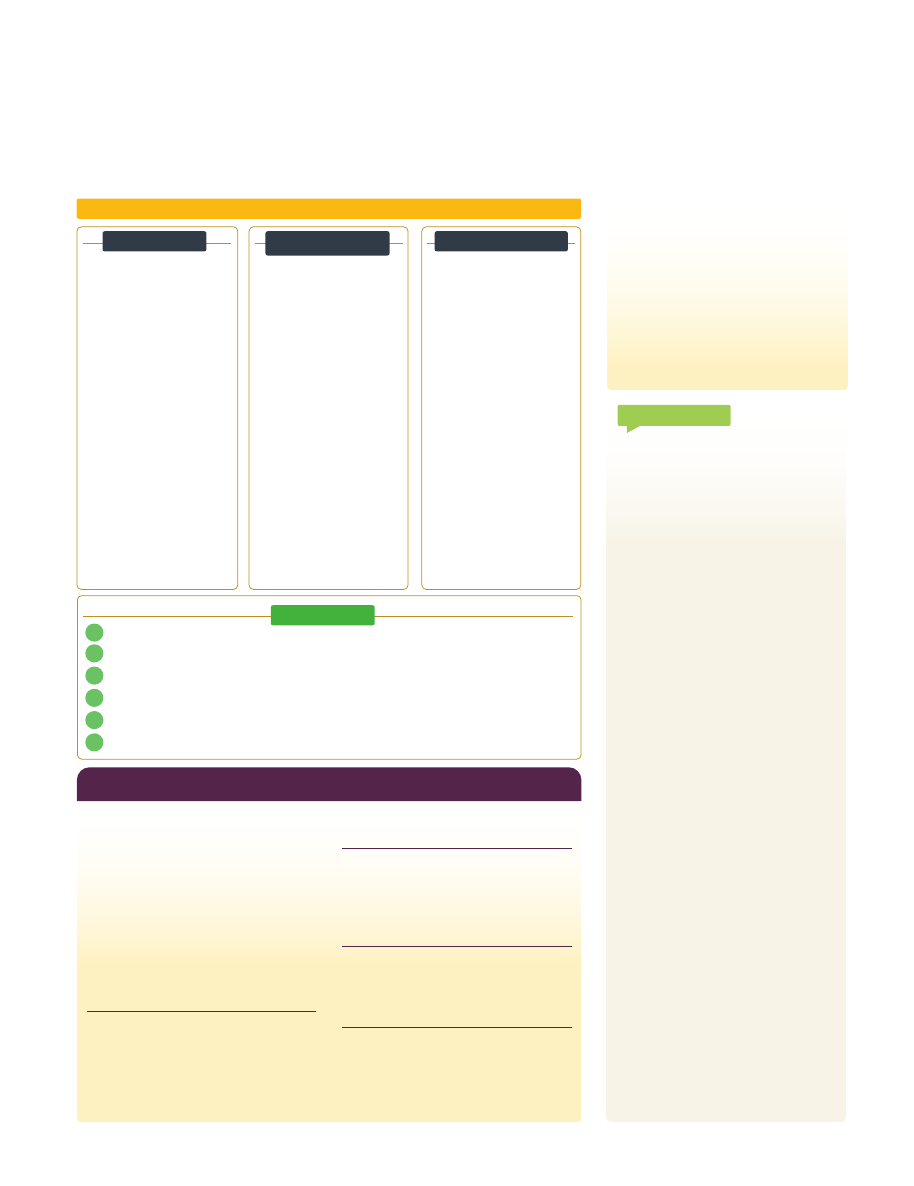

Enterprise Risk Management

(ERM) Framework

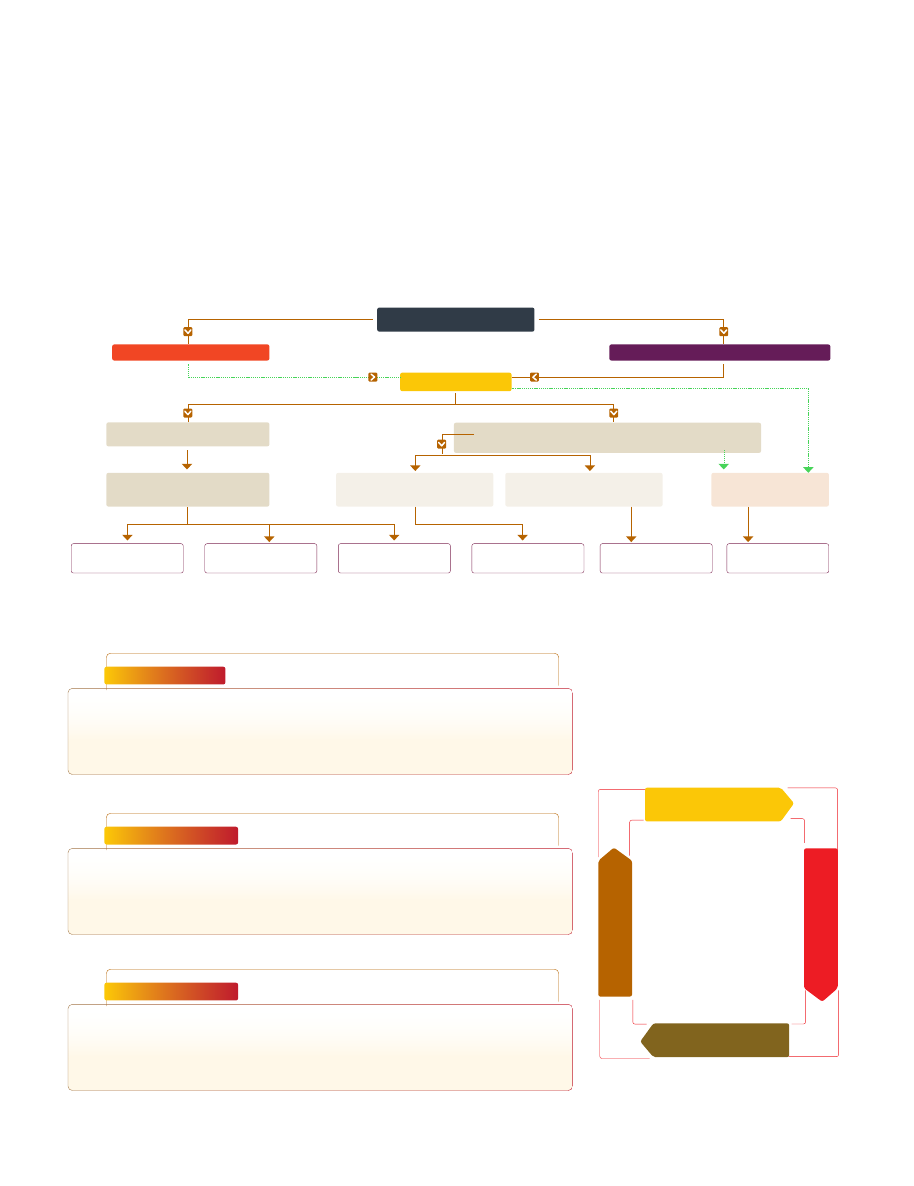

The Board approved risk management framework consists of clearly-defined governance structures, policy frameworks and a culture of risk awareness which ensures management of risks across the Bank. Risk management framework provides comprehensive guidelines to identify, measure, mitigate, and report risks in a consistent manner. Risk management framework is regularly reviewed and revised to ensure that it remains relevant, given the increasingly dynamic operating environment.

In response to significant changes to the operating environment and newly- introduced internal processes, the Bank reviewed and updated all policies in 2023. Considering the complexity of the stressed operating environment, the Bank has widened the scope of monitored risks to increase focus on liquidity, interest rate and environmental and social risks.

INDEPENDENT

INTEGRATED

RISK MANAGEMENT

DIVISION (IIRMD)

Objectives

•

Enhance the Bank’s ability to anticipate and mitigate risks effectively while maximising opportunities for growth.

•

Establish common policies and standards for the management and control of all risks.

•

Provide a common language, system and framework to foster a consistent approach to manage risks.

Executive Committee Fraud Risk Management Committee Committee Dealing with Operational

Losses Business Continuity Management

Committee

Information

Security

Corporate Information Security Committee

Risk related Board

Committees

Integrated Risk

Management

Committee (IRMC)

Audit

Committee

Information and

Communication Technology

Committee

General Manager

Board of Directors

First line of defence

Second line of defence

Third line of defence

Business Units

Independent Integrated Risk

Management Division (IIRMD)

Internal

Audit

1

2

3

Risk Appetite, Culture and Management

Credit Risk

Management

Policies

Integrated Risk

Management

Policy

Market Risk

Management

Policies

Group Risk

Management

Policy

Liquidity Risk

Management

Policies

Stress Testing

Policy

Operational Risk

Management

Policies

Integrated Environmental and

Social Management System Policy

Information

Security and IT

Risk Management

Policies

ICAAP Policy

Overseas

Branches Risk

Management

Framework

RISK GOVERNANCE AND OVERSIGHT

The Board of Directors holds ultimate responsibility for managing the Bank’s risks within the defined parameters set out in the risk appetite. The Integrated Risk Management Committee (IRMC) supports the Board in its oversight of risk management and related duties and the Independent Integrated Risk Management Division (IIRMD) ensures that the risk management process is carried out effectively.

Board of Directors

Chief Risk Officer

General Manger

AGM (Credit Risk Management)

AGM (Market Risk and Operational Risk Management)/

Data Protection Officer

Chief Manager

(Market Risk Management)

Chief Manager

(Operational Risk Management)

CISO

Chief Manager

(Credit Risk Management)

Integrated Risk Management Committee

Credit Quality

Assurance

Credit Risk

ESMS

Market Risk

Operational Risk

IS/IT Risk

The three lines of defence mechanism serves as the basis of enterprise-wide risk governance and oversight supported by clear division of responsibilities.

•

Proactive identification, assessment and measuring of risks. The First Line also manages day-to-day transactions and portfolio level risks within the limits specified by the risk appetite framework, related policies and guidelines.

Risk taking and ownership

by business units

First line of defence

1

•

Development and execution of the risk management framework while setting the risk appetite and establishing the risk culture throughout the organisation. Providing guidance and support to the first line of defence and the management on risk-related activities.

Risk management, control and

oversight by the IIRMD

Second line of defence

•

Provides independent and objective assurance to the Board on the effectiveness and adequacy of risk management and internal controls.

Assurance by internal audit

Third line of defence

2 3

RISK MANAGEMENT PROCESS

With clearly delineated roles and responsibilities, well-defined policies, procedures, and processes; the Bank’s ERM framework supports consistent identification and management of risks across business units, functions, and operations.

Comprises of four members of which three are independent

Non-Executive Directors.

The Division operates independently and is headed by the

Chief Risk Officer (CRO)

Responsibil

ities

•

Assist the Board in discharging its oversight responsibilities for risk management.

•

Ensure that appropriate policies and procedures are in place for detection, oversight and analysis of existing and future risks.

•

Ensure the Bank’s risk management activities are aligned with the Bank’s risk appetite.

•

Assess all risks to the Bank on a periodic basis through appropriate risk indicators and management information.

•

Provide strategic guidance on various initiatives undertaken by the Bank towards management and mitigation of credit, market, operational and information security risks of the Bank.

•

Review the Bank’s capital position and future requirements in line with the Internal Capital Adequacy Assessment Process (ICAAP) while identifying and mitigating potential pain points highlighted in stress testing.

•

Review the Bank’s Business Continuity Plan.

•

Re-enforce the culture and awareness of risk management throughout the organisation.

•

Coordinate the organisation’s Enterprise Risk Management system.

•

Responsible for understanding the risks assumed by the Bank and ensure that the risks are appropriately managed.

•

Review the risk profile, envisage future challenges and threats and prioritise action steps to mitigate the potential risks.

•

Determining the Bank’s Risk Appetite, including defining specific key risk indicators, ensuring appropriate monitoring and reporting mechanism in place.

•

Support the business units and inculcate risk culture through continuous training and awareness.

•

Ensuring regulatory compliance to ICAAP, BCP and RCP requirements.

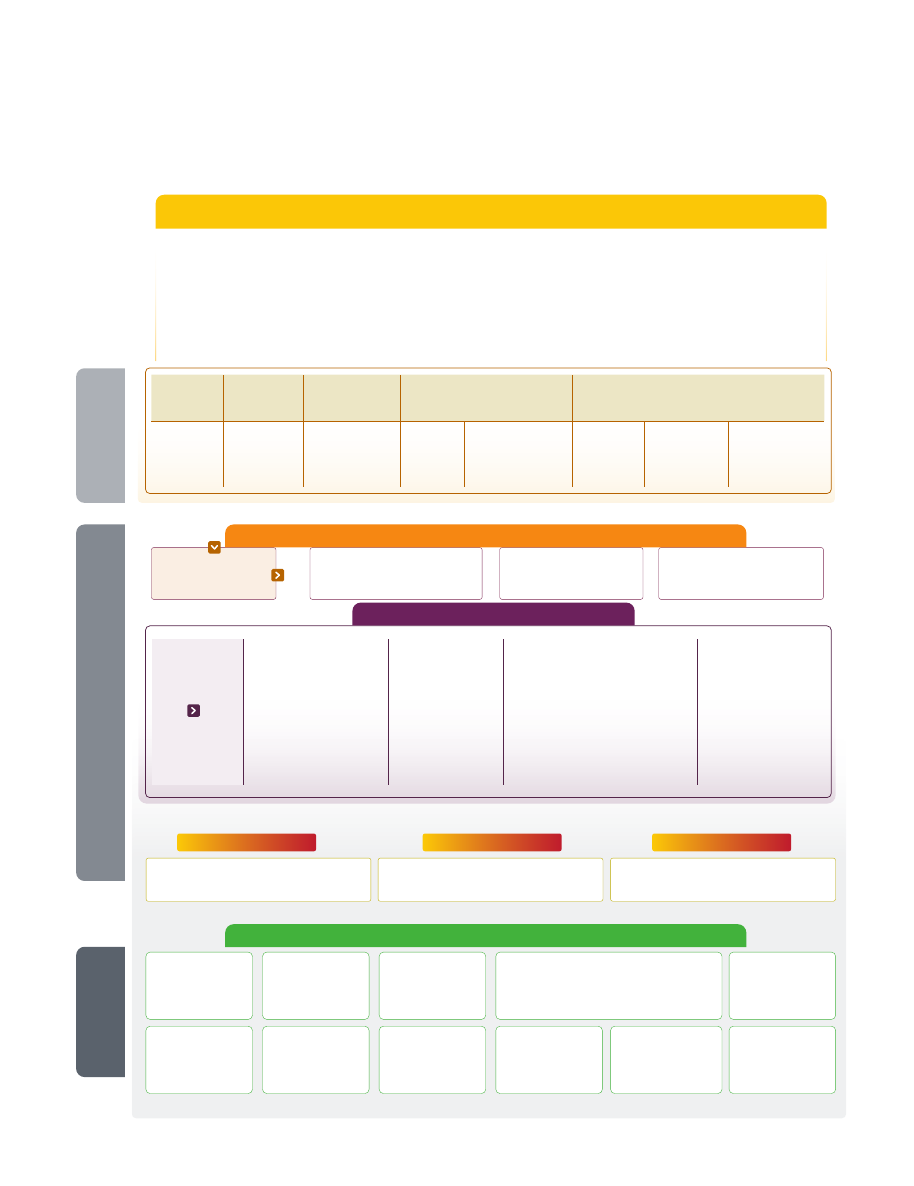

Risk category

Key risk indicator

Regulatory requirement

/policy parameter

Actual

position

31.12.2023

31.12.2022

R1

Credit risk

Asset quality

Net Stage 3 loans ratio (%)

5.07

5.27

Impairment Coverage (Stage 3) Loans ratio (%)

60.44

59.73

Concentration

and exposure

Sector-wise concentration (HHI)

991

999

Geographical concentration

2,031

2,062

R2

Market risk

Net Interest Income (NII) (LKR million)

91,188

126,346

Net Interest Margin (NIM) (%)

2.08

3.10

Price Value Per Basis Point (PVBP) of Treasury Bonds

577,985

75,767

R3

Liquidity risk

Liquid asset ratio (LCY) (%)

20.00

42.80

21.22

Liquid asset ratio (FCY) (%)

20.00

53.63

32.79

Liquidity Coverage Ratio (LCR) (%)

100.00

227.71

122.77

Net Stable Funding Ratio (NSFR) (%)

100.00

145.00

139.00

Credit-Deposit (CD) ratio (%)

63.38

77.58

R4

Strategic risk

Tier 1 Capital Ratio (%)

10.00

12.76

12.41

Total Capital Ratio (%)

14.00

15.84

15.38

Common Equity Tier 1 Ratio (%)

8.50

11.71

11.34

RoE (%)

10.55

14.06

R5

Operational Risk

Operational loss as a percentage of risk appetite (%)

7.00

82.00

THE BANK’S APPROACH TO RISK

MANAGEMENT

Bank of Ceylon’s risk management function centres around an Enterprise Risk Management (ERM) framework that ensures risks are managed within a framework aligned to the Bank’s strategic priorities, organisational culture and corporate governance practices.

The Board approved risk management framework consists of clearly defined governance structures, policy frameworks and a culture of risk awareness which ensures judicious empowerment and the consistent management of risks across the Bank.

The framework provides comprehensive guidelines to identify, measure, mitigate, and report risks in a consistent manner and is regularly reviewed and revised to ensure that it remains relevant given the increasingly dynamic operating environment.

In 2023, the Bank brought forward new systems, processes and protocols in response to the changing and challenging operating environment. Focus was placed on Information Security Risk Management in light of continued digitalisation and adoption of new systems instituted.

The Bank continuously works to improve its Environmental and Social Management System, ensuring it is in line with international best practices, related legal provisions of the country and the Sustainable Finance Initiative of the Central Bank of Sri Lanka (CBSL).

Looking to the future, Bank of Ceylon expects to strengthen baseline security alongside stringent Information Security Risk Management to ensure alignment with the direction of Sri Lanka’s economy and the financial sector.

Risk Appetite and Tolerance Limits

Risk appetite and tolerance limits are used to align business planning and decision making processes in order to ensure pursuit of strategic objectives is within the maximum amount of risk the Bank is willing to accept.

Risk appetite

• Refers to the extent and type

of risk the Bank is willing to take to meet strategic objectives

Risk tolerance

• Describes the level of

uncertainty the Bank will accept and identifies the maximum risk boundary, beyond which the Bank is unwilling to operate

Risk appetite statement of the Bank is continuously monitored and reviewed at least annually, considering the volatilities in capital base, macroeconomic changes, country and counterparty risk, expected business growth and the corporate plan.

Stress testing

The stress testing framework of the Bank has been prepared in line with regulatory guidelines and international best practices, utilising a combination of techniques including macroeconomic and business model stress testing along with sensitivity and scenario analysis. It covers all the material risks such as credit, market, operational, concentration, liquidity, foreign exchange and interest rate under three different stress levels: mild, moderate and severe.

Regular stress testing evaluates potential effects on the Bank’s business and assesses sensitivity of the current and potential risk profile relative to risk appetite. The impact on the profitability, liquidity and capital is assessed, evaluated and reported to the top management and IRMC on a monthly basis and case-by-case basis for effective

decision making. Stress testing also contributes to increase risk awareness across the Bank’s functions and works to safeguard business continuity by means of proactive management. Furthermore, it supports setting up of the risk appetite and tolerance limits, risk identification and control, complementing other risk management tools, development of contingency plans, improving capital and liquidity augmentation in achieving the strategic business objectives. A comprehensive stress testing provides a broader view to the regulator, external rating agencies and Multilateral Development Banks (MDBs) on resilience of the Bank in internal and external stress situations as a Domestic Systemically Important Bank (D-SIB).

In light of the changes in the operating environment, adequacy and frequency of stress tests, shock levels and assumptions were critically reviewed and changes were incorporated as required.

The Bank proactively and comprehensively evaluated the impact of debt restructuring (haircut on investment securities, both domestic and foreign) under different scenarios and different stress levels given the non-availability of specific conditions. Further impact of possible restructuring of State-Owned Enterprises (SOEs) and the impact emanating from the Bank diagnostic exercise are stresses amongst the full range of stress testing scenarios. The resultant impact of such analysis comforts the Bank's decision-making process, that enabled revisiting and revising of pricing mechanism, adequate impairment provisioning for potential risks and searching for alternative funding avenues.

The Bank’s stress testing reports have been presented to the regulators and external funding agencies who have provided a satisfactory response on the outcome of our stress tests.

RISKS AND OPPORTUNITIES

RISK CULTURE

The Bank’s risk culture starts with leadership, with senior management setting the tone from the top by demonstrating a commitment to risk management, compliance, and ethical conduct. The robust risk culture promotes risk awareness and education at all levels of the Bank, ensuring that employees understand their roles and responsibilities in managing risk effectively.

Training programmes, workshops, and communication initiatives in the areas of strong credit culture, E&S risk management, information security, market and operational risk management helped to raise awareness on risk management practices, regulatory requirements and emerging risks within the industry complementing the first line of defense.

The risk culture extends beyond the boundaries of the Bank to encompass interactions with all stakeholders, including regulators, investors, customers and counterparties. Building trust, transparency and credibility with external stakeholders through ethical conduct, regulatory compliance and responsible risk management practices enhance the Bank’s reputation and resilience while sustaining long-term value creation.

Capital management and Internal

Capital Adequacy Assessment

Process (ICAAP)

Proactive management of the capital position, capital mix and capital allocation is a crucial aspect of risk management in order to safeguard the Bank’s financial position and reputation not withstanding the capital requirements set as per the regulations. The Bank’s approach to capital management is driven by its strategic objectives and is aligned with the Pillar II requirements.

The Internal Capital Adequacy Assessment Process and Recovery Plan (ICAAP and RCP) Steering Committee is responsible for assessing and managing the risks associated with the Bank’s capital management and developing the capital augmentation plan.

The Bank focused on strengthening capital buffers through internal capital generation and through the issuance of listed BASEL III compliant Tier 2 debentures (LKR 10 billion), considering the recapitalisation needs arising with the domestic debt optimisation, restructuring of foreign currency exposures of SOEs and forward-looking impact assessments despite the current comfortable level of capital position and buffers.

Recovery Plan (RCP)

The Recovery Plan provides the framework for Bank’s governance, identification of credible options to survive a range of severe but plausible stress scenarios arise from institution- specific stresses, market-wide stresses, or a combination of both and sets out the plan for profitability, liquidity and capital management arrangements while improving the risk profile and ensuring the business continuity. RCP causes a predetermined escalation and information process up to top management within the Bank and its supervisory authority in a trigger situation. ICAAP and RCP committee is the executive committee responsible for implementation and execution of the recovery plan in the Bank.

The RCP is integrated with the Bank’s

•

Strategic, risk management and business decision making processes

•

Capital and funding planning, stress testing approaches and business continuity planning

•

Capital and liquidity assessments

•

Risk data aggregation and risk reporting

Under RCP, triggers and early warning indicators are set based on the capital, liquidity, profitability, asset quality and market & macroeconomic indicators. The Risk indicators set as alerts and triggers are monitored regularly and the precautionary actions are taken before a trigger occurs. However, the breaching of a trigger at any time will activate the Recovery Plan of the Bank.

Given the stress on Net Interest Margin (NIM) of the Bank during the year 2023, the ICAAP and RCP Steering Committee activated range of recovery options resulting in gradual improvement in the ratio under the scrutiny of the regulator. Therefore, a comprehensive RCP plays a pivotal role in restoring the financial position and market confidence in Bank's resilience following an adverse shock which will ensure interest of all the stakeholders are safeguarded.

Risk reporting

Under the challenging operating environment which prevailed during the year, risk reporting to the Board via Integrated Risk Management Committee further strengthened with measures taken to improve the processes of providing timely, accurate and comprehensive risk information. Special emphasis was placed on credit, liquidity, operational, interest rate risk and information security related risks, risk interdependencies, and potential risk mitigation strategies.

Broad analysis and reporting of emerging risks on regular basis and submission of comprehensive monthly risk report, comprising risk dashboards to the IRMC, strengthened the risk management oversight.

The Bank provides quantitative and qualitative disclosures in line with the BASEL III requirements as specified by the regulator through the Annual Report, website and printed media in order to provide a meaningful assessment of risks confronted by the Bank.

KEY DEVELOPMENTS IN 2023

CREDIT RISK

Bank utilised its risk management framework in line with three lines of defense model to manage and mitigate credit risk successfully during the year. Emphasis was on the strengthening first line of defense, maintaining asset quality, supporting the business growth in line with the Bank’s risk appetite.

GOVERNANCE

The Board holds apex responsibility in ensuring the Bank's credit risk exposures are managed within the defined risk appetite. The IRMC is responsible for implementing Bank's credit risk management framework while supporting the Board in its oversight to credit risk management related duties.

Credit Committee

Credit Risk Management Unit

•

Formulating, reviewing, and implementing credit risk appetite limits

•

Approving/recommending credit proposals within authorised limits

•

Ensuring regulatory compliance in the Bank's risk policies and guidelines

•

Recommending credit related policies

•

Monitoring risk concentrations

Provides independent review of the first line of defence. Manages and oversees Bank-wide credit risk management

Carries out periodic post-sanctioning review of large credit exposures

Identifies and manages the Bank’s exposure to the environmental and social risks of its

lending portfolio

Credit Quality Assurance Unit

ESMS Unit

POLICY FRAMEWORK AND METHODOLOGIES

Pre-credit sanctioning

Post-credit monitoring

Credit risk management framework

The Bank's comprehensive Credit Risk Management Policy mandates the following pre- credit sanctioning and post-credit monitoring mechanisms

•

Structured credit appraisal mechanisms and defined credit criteria

•

Multiple levels of approval authority and independent review by CRO

•

Limits for credit risk categories such as default, concentration and counterparty

•

Retail scorecards and borrower rating models

•

Risk based pricing

•

Regulatory limits

•

Ongoing and robust credit review

•

Portfolio evaluation

•

Proactive engagement with customers in identifying requirements and stresses

•

Stress testing and scenario analyses

•

Monitoring watch list exposures

•

Ensuring loan review mechanism by Credit Quality Assurance Unit

•

Early warning signals

•

Supported the revival and resumption of economic activities.

•

Successful Bank-wide rollout of the Environment and Social risk assessment in lending activities.

•

Strengthened the process of post sanctioning review through credit quality assurance units.

•

Comprehensive review of credit risk management policies.

ESMS

The Bank successfully rolled out its Environment and Social risk assessment guidelines in line with its Integrated Environmental and Social Management System Policy, which outlines the procedures for identifying, assessing and managing environmental and social risks of financial transactions. While supporting the growth of products to promote sustainable green financing and financial inclusion, the Bank’s ESMS entwined with ESG considerations, ensures that its lending activities and operations are environmentally and socially responsible and compatible with the applicable regulatory environmental and social standards, country regulations as well as globally recognised best practices.

In support of Sri Lanka’s Sustainable Finance Roadmap, BoC identifies and evaluates associated climate related risks and green financing activities in its lending portfolio. With the focus of promoting sustainable and environmentally friendly infrastructure to customers, the Bank through Environmental and Social Due Diligence (ESDD) procedures, identifies opportunities that could contribute to greener and more sustainable economy in Sri Lanka.

RISKS AND OPPORTUNITIES

Opportunities

Enhance financial intermediation

Create a robust ecosystem that efficiently channels funds, manages risks, and supports economic growth.

Improve green financing

Develop green finance products and lending portfolio which supports sustainable development while addressing climate challenges.

Increasing exposure to the private

sector

Further diversify Bank's portfolio while supporting the economic growth of the country.

GEOGRAPHICAL CONCENTRATION

%

4.1%

1.4%

0.5%

3.2%

0.4%

0.1%

3.3%

5.2%

3.9%

9.3%

60.1%

42.1%

2.9%

3.3%

4.2%

3.7%

2.0%

2.3%

4.1% 4.0%

•

Westen Province

•

Overseas Branches

•

Offshore Banking

•

Uva Province

•

Sabaragamuwa Province

•

North Western Province

•

North Central Province

•

Eastern Province

•

Northern Province

•

Central Province

•

Southern Province

•

Corporate

•

Metro

•

Pettah

•

Head Office

•

Card Centre

•

Islamic Banking

•

Western Province North

•

Western Province South

•

Western Province Central

COLLATERAL

CONCENTRATION

%

4.1%

1.7%

7.3% 1.2%

28.4%

4.2%

53.1%

•

Cash

•

Gold

•

GoSL Securities/Guarantees

•

Movables

•

Property

•

Others

•

Unsecured

RATING GRADE-WISE

DISTRIBUTION

%

11%

89%

•

AAA to BB

•

B and Below

CROSS BORDER EXPOSURE

OF THE BANK

%

93.4%

1.7%

0.7%

0.3% 1.1%

0.1%

2.7%

6.6%

•

UK

•

India

•

USA

•

Other Countries

•

Seychelles

•

Maldives

•

Other Assets

•

Cross border

Assets

SECTOR

CONCENTRATION

%

11.0%

3.5%

16.1%

2.4% 2.0%

40.3%

9.8%

5.2% 6.5% 3.2%

•

Agriculture and Fisheries

•

Banks, Financial, Insurance and Business Services

•

Hotels, Travels and Services

•

Housing, Construction and Infrastructure

•

Manufacturing

•

Commercial Trade

•

Sovereign and Direct Government

•

Transportation and Logistics Services

•

Other Commercial Services

•

Consumption and other

Improve asset quality through revival

and rehabilitation

Providing support to businesses to withstand negative impacts of the economic conditions in the aftermath of the pandemic.

Process improvement through digital

adoption

Enhance credit management process via evolving digital adoption.

Facilitate economic development

financing key sectors

Supporting more inclusive and resilient growth of country's economy utilising the Bank's financial strength to facilitate capital allocation for key sectors.

RISKS AND OPPORTUNITIES

PRODUCT-WISE

CONCENTRATION

%

7.8%

3.0%

28.0%

1.2%

0.3% 15.4%

24.4%

3.0%

4.7%

0.7%

6.6%

1.1%

3.4%

0.4%

•

Trade Finance

•

Ran Surakum

•

Leasing

•

Staff Loans

•

Loans under Schemes

•

Overdrafts

•

Credit Cards

•

Housing Loans

•

Foreign Currency Loans Others

•

Term Loans

•

BoC Personal Loans

•

Pledge Loans

•

Money Market Loans

•

Loans Others

MARKET RISK

Market risk is the adverse variation around expectation and arises due to negative movement in variables such as interest rates, exchange rates, share prices and commodity prices. Market risk arises through the banking book and the trading book and comprises the following:

Risk type

Management tools and indicators

Interest Rate Risk

(IRR) – arising from

the Bank’s trading

and non-trading

books

•

Maturity mismatches, interest rate gaps and Price Value per Basis Point (PVBP) are monitored on a consistent basis.

•

Implications of changes in macroeconomic conditions are assessed through regular stress testing.

•

Stress testing on interest rate movements

Foreign exchange

risk – stemming from

foreign currency

denoted transactions

•

Forex transactions are governed by stringent internal policies, including approval mechanisms, external regulatory guidelines and limits set by the Bank and the regulator.

•

Internally, a comprehensive limit structure, comprising Value at Risk (VaR) limits and volume limits for open positions of both individual and aggregate currency exposures, are used to manage vulnerabilities.

•

Stress testing on plausible forex risk scenarios.

Equity risk – losses

from volatilities in

equity prices

•

A dedicated investment committee is in place to ensure that the Bank’s investment decisions are in line with the Board’s expectations on risk-return dynamics.

•

The market risk division ensures the limit structure is in place for proper management of the equity portfolio.

•

Comprehensive stress testing.

GOVERNANCE

The Board provides directions with respect to market risk management framework and oversees that all aspects of market risk is managed. As Board level subcommittee, IRMC supports the Board in its oversight of risk management and related duties.

The Asset and Liability Committee (ALCO) and investment committee holds the responsibility of managing the Bank’s market risk and makes recommendations to the IRMC.

Market risk refers

to the potential

for financial losses

arising from adverse

movements in

market variables such

as interest rates,

foreign exchange

rates, equity prices,

commodity prices,

and other relevant

financial indicators.

Asset and Liability Management

Committee (ALCO)

Treasury Middle Office/Market Risk

Management Unit

•

Analysing market risk associated with financial markets and recommending mitigation actions

•

Recommending and approving market risk limits within delegated authority

•

Overseeing various enterprise-wide market risk exposures

•

Recommending the appropriate pricing structure

The middle office at IIRMD independently reviews the treasury operations.

The middle office functions of treasury operations are governed primarily through market risk management policies and limit management framework.

POLICY FRAMEWORK AND METHODOLOGIES

Market risk management framework

The Bank's market risk management framework recognises the importance of robust risk management practices and is based on clearly defined governance structure, strategies, risk mitigating tools and procedures to identify, quantify, measure and manage market risk.

Key elements of the Bank's market risk management function

Market risk policies

Risk limits

Risk monitoring

The Market risk policy framework comprises the following:

•

Market risk management policy

•

Limit management framework

•

Foreign exchange risk management policy

•

Middle office operations manual

Policies are reviewed and updated regularly by the Board in view of changing dynamics in the operating landscape.

Risk limits are set for treasury and investment related activities including foreign currency open position limits, counterparty limits, stop loss limits and dealer limits.

The Board holds ultimate responsibility for this exercise and is supported by the ALCO.

Limits are regularly reviewed and updated by the IIRMD (with input from the ALCO) in line with market developments.

Market risk is monitored through a range of indicators including interest margins, foreign currency exposures, equity exposures, and funding requirements.

The monitoring mechanism is supported by tools such as value at risk, price value per basis point, duration, gap analysis, stress testing, sensitivity analysis, limits, and net open positions.

KEY DEVELOPMENTS IN 2023

•

Implemented additional monitoring mechanisms for Treasury Operations.

Expanded the monitoring domain by incorporating several additional risk parameters to improve the effectiveness of monitoring mechanism and enrich the reporting. The following risk parameters were included into daily monitoring procedure:

1

Off market exchange rates

2

Forward exchange contracts

mismatch limits

3

Intraday open position limit

4

Pre-settlement risk limits of

fixed income securities with counterparties

Daily risk report was enriched with those additional risk parameters, in order to enhance the scope of the reporting to the management.

•

Provided risk insights to improve the Net Interest Margin (NIM) of the Bank.

The following areas were broadly addressed to improve the NIM of the Bank.

1

Adjustment of interest rates

in line with policy rates and structure of the assets and liabilities

2

Focusing the Net Interest

Income of FCY assets and liabilities

3

Reduction of non-interest

earning assets

4

Use of variable rates

mechanisms for improving NIM

5

Finding new hedging methods

to curtail interest rates risk

6

Improvement of CASA

Opportunities

•

Bank foresees some opportunities to improve the liquidity and profitability using new trends in the market space. Specifically, with reducing interest rates scenario and gradual improvement of foreign exchange liquidity in the economy. Bank has the opportunity to align its mechanisms of Asset and Liability Management to have a better margins with reducing interest rates and better exchange gains through increased foreign exchange transactions like exports, imports and retail foreign exchange conversions.

RISKS AND OPPORTUNITIES

MATURITY ANALYSIS OF ASSETS AND LIABILITIES - DECEMBER 2023

SENSITIVITY ANALYSIS OF ASSETS AND LIABILITIES DECEMBER 2023

•

GAP %

•

Rate sensitive liabilities %

•

Rate sensitive assets %

-5.00%

0

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

Over 5 Years

4-5 Years 3-4 Years 2-3 Years 1-2 Years

6-12 Months

3-6 Months 1-3 Months

Upto 1 Month

%

PVBP T Bond

LKR

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

Jan.

23

Feb.

23

Mar.

23

Apr.

23

May.

23

Jun.

23

Jul.

23

Aug.

23

Sep.

23

Oct.

23

Nov.

23

Dec.

23

•

T bond

PVBP T bond limit

LIQUIDITY RISK

Liquidity risk involves potential losses to earnings and/or capital due to inability to meet the Bank’s financial obligations as and when they are due. The Bank’s liquidity risk management framework ensures the effective management of day-to-day liquidity risk and Bank's resilience in facing unexpected liquidity crisis conditions.

Asset and Liability Management Committee (ALCO)

•

Consistent monitoring of the liquidity profile to ensure compliance to regulatory requirements and internal targets

•

Formulating a contingency liquidity plan

•

Exploring avenues of bridging liquidity shortfalls and alternative funding arrangements

•

Recommending relevant risk appetite limits

•

Evaluating stress testing and making recommendations

POLICY FRAMEWORK AND METHODOLOGIES

Liquidity risk management framework

Liquidity policies

Liquidity measurement

Contingency Funding Plan

Policies such as Liquidity Risk Management and Asset and Liability Management provide guidance on mechanisms, tools, and stress testing methodologies that are to be adopted in managing liquidity risk exposures.

Flow approach: Assessment of projected/ actual inflows and outflows in time buckets.

Fund approach: Measures liquidity position through liquid assets ratio, liquidity coverage ratio, net stable funding ratio and credit to deposit ratio etc.

The plan defines specific triggers and action plans with responsibilities to ensure business continuity in the event of liquidity stress.

GOVERNANCE

The Board oversees the establishment and approval and reviewing of liquidity management strategies, policies and procedures while its delegated subcommittee, the IRMC supporting the Board in its oversight of liquidity risk management.

The Asset and Liability Management Committee (ALCO) as the responsible management committee for monitoring and managing the liquidity risk of the Bank, carries out the required evaluations and makes recommendations to the IRMC on the relevant risk appetite limits.

KEY DEVELOPMENTS IN 2023

•

Recorded a significant increase in the foreign currency liquidity position mainly as a result of the migrant worker remittances.

•

Stringent Management of Foreign Currency liquidity through prioritised payments.

•

Improving CASA

Opportunities

•

With gradual improvement of FCY liquidity in the market, the Bank has opportunities of mobilising FCY deposits at low cost

•

With gradual recovery of the economy create more borrowing opportunities to handle liquidity stress situations

•

Contingent Funding Plan of the Bank will help to ease the liquidity stresses

UNENCUMBERED SECURITIES

LKR

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

•

2023

•

2022

OPERATIONAL RISK

Operational risk is defined as the risk of loss resulting from inadequate or failed internal processes, people and systems or from external events such as natural disasters. The Bank’s operational risk management is guided by the operational risk management framework which supports the identification, measurement, management, monitoring and reporting of material operational risks.

GOVERNANCE

The Board is primarily responsible for ensuring effective management of operational risk within the Bank. The IRMC is responsible for implementing the Bank's operational risk management framework while supporting the Board through oversight on operational risk management related duties.

Risk identification and management is done through the Operational Risk Management Executive Committee (ORMEC) and provincial operational risk management committee. The ORMEC along with the fraud risk management committee and the operational risk management unit report to the IRMC.

Operational Risk Management

Executive Committee (ORMEC)

Fraud Risk Management

Committee (FRMC)

Operational

Risk Management Unit

Key responsibilities

•

Assists the IRMC

to discharge its

statutory duties and

its responsibilities in

relation to operational

risk management of the

Bank

•

Operational risk strategy

and policy development

and review

•

Monitor and ensure that

appropriate operational

risk management

framework is in place

•

Discuss and recommend

suitable controls/

mitigant for managing

operational risk

•

Ensuring a mechanism is in place to record

operational loss events

and near misses, and

ensuring that action is

taken within reasonable

time

•

Formulation of

coherent and

consistent responses

to developments in the

external operational

environment

•

Coordinated responses

to interdepartmental

and inter business units

•

Review and approve

the development

and implementation

of operational risk

methodologies and

tools

Key responsibilities

•

Identify the systemic

gaps if any that

facilitated perpetration

of the fraud and

recommend measures

to plug the same

•

Identify the reasons for

delay in detection of

risk, if any, reporting to

top management of the

Bank

•

Ensure that staff accountability is

examined at all levels in

all the cases of frauds

and staff side action, if

required, is completed

quickly without loss of

time

•

Monitor progress of

Bank/ CID/ Police

Investigation, and

Recovery position

•

Review the efficiency

of the remedial action

taken to prevent

recurrence of frauds,

such as strengthening of

internal controls

•

Recommend any other

measures as may be

considered relevant to

strengthen preventive

measures against frauds

Key responsibilities

•

Co-ordinating and managing all the

operational risk activities

of the Bank and working

towards achievement

of the stated goals and

objectives

•

Formulating all the

operational risk related

policies and ensuring

their review as per

timelines

•

Implementing tools

related to operational

risk management such

as Risk and Control Self- Assessment (RCSA), Key

Risk Indicators (KRIs),

Loss Data Management

etc., and working

towards the goals of

improved controls and

lower risk

•

Product/ process

reviews for operational

risk mitigation

•

Co-ordinates with the HR department to

ensure regular trainings

are provided to the

Bank’s employees to generate awareness

about operational risk

manag

ement

RISKS AND OPPORTUNITIES

Tools and mechanisms

Policy framework

Risk identification and

measurement

Reporting and monitoring

Key policies include:

•

Operational Risk

Management Policy

•

Fraud Risk Management Policy

These are clearly set out guidelines on responsibilities, tools, and procedures in the identification, assessment, mitigation and monitoring of operational risks.

Risk and Control Self Assessment (RCSA) framework of the Bank enable identification of operational risks that may arise from business objectives, products and services and operational procedures. The control effectiveness over those risk is evaluated, tested and monitored for critical business units.

Key risk indicators, internal loss data incident reporting and root cause analysis are also used to evaluate exposure to operational risks.

The IRMC and the Board are regularly updated on operational risk events/ losses and control failures.

The Bank also maintains a database of operational losses and incidents allowing identification of trends in operational risks and root causes. As an organisation-wide risk exposure, the Bank strives to nurture a risk conscious culture by encouraging employees to share knowledge.

Mitigation

1

Robust internal control structure

2

Business Continuity Plans for all critical business units and support functions

3

State-of-the-art disaster recovery centre

4

Comprehensive insurance cover

5

Ongoing process evaluation for improvements

6

Creating a culture of risk awareness

KEY DEVELOPMENTS IN 2023

•

Reinforced the risk assessment process of overseas branches through introduction of a comprehensive questionnaire to ensure that an appropriate Operational Risk Management Framework is in place under the course of continuous endeavors of IIRMD to proactively identify and mitigate potential risks across Bank’s global operations.

•

Improved process controls through

Risk and Control Self-Assessment (RCSA) in critical units in the Bank

which ensures a single standard

for risk and control that facilitates

management oversight, optimises

resource utilisation and meets the

regulatory requirements.

•

Reviewed and improved the checklist of the Branch risk assessment which complement the effective functioning of the provincial ORMC.

•

Provided a risk perspective when introducing a new product/process and review existing products/ processes.

•

Effective usage of ‘tvBOC’ to carryout awareness programmes to all levels of staff especially to Managers and Internal Control

Officers focusing on arresting loss events.

•

Revamping Bank-wide circulars: A special task is carried out by the BPRP unit with the feedback and analysis from IIRMD and other stakeholders to refurbish the Bank- wide circulars as a Bank with over eight-decade history.

Opportunities

• Initiation of projects to drive

automation:

Automation of monitoring mechanism will collect around the clock data and fill into reports automatically that enables comprehensive analysis and identification of issues in the processes that have not been noticed before. This also helps to remove the vast majority of human error from processes.

• Improved control environment

Improved control environment ensures that the processes are not just compliant but also efficient specially in the journey of digital transformation. Internal circulars are a highly-effective way to communicate with employees and revamping of Bank-wide circulars will streamline the internal control mechanism throughout the Bank.

• Training and awareness

Effectively functioning training department, well-equipped centralised training institute and a Bank-owned internal TV channel complement the employee development in many ways. Enhancing of employee productivity and improving the Bank’s culture are amongst continuous efforts to strengthen work performance and a controlled operational environment.

POLICY FRAMEWORK AND METHODOLOGIES

RISKS AND OPPORTUNITIES

LOSS EVENT TYPE

DISTRIBUTION FOR YEAR 2023

%

1%

61%

14%

15%

•

Execution, Delivery and Process Management

•

External Fraud

•

Clients, Product and Business Practices

•

Internal Fraud

•

Business Disruption and System Failures

9%

RISK APPETITE VS ACTUAL

LOSSES AND PROVISIONS

LKR million

0

200

400

600

800

1,000

1,200

1,400

Risk Appetite

Jan.

23

Mar.

23

Jun.

23

Sep.

23

Dec.

23

Losses written off and Provisions made

INFORMATION SECURITY

AND TECHNOLOGY RISK

Information Security and Technology Risk involves the risk of loss or theft of information, data and money, or potential service disruption stemming from the adoption of IT within the Bank. Cyberattacks, phishing scams, and ransomware incidents are on the rise, posing significant challenges to IT infrastructure, customer data security, and operational resilience. Having understood the criticality of proactively addressing these threats, the Bank continued to invest in updating its digital defences.

KEY DEVELOPMENTS IN 2023

•

In addition to the Information Security Policy that was already in place, the Bank introduced and implemented the Cyber Security Policy

•

Commenced implementation of the COBIT 2019 Framework under the leadership of the Chief Risk Officer. We are the first bank in Sri Lanka to adopt this globally accepted IT governance framework, which will align existing frameworks and processes with the Bank’s overall strategy and strengthen the governance of information security, compliance and risk management

•

Completed risks assessments in alignment with ISO 27001

GOVERNANCE

Corporate Information Security

Committee (CISC)

•

Provide management direction and support for the Information Security (IS) initiatives

•

Ensure the establishment of the Information Security objectives and plans in line with business objectives

•

Ensure the application of processes and procedures specified in the Information Security Policy (ISP)

•

Review and communicate the information security plans and programmes to maintain information security awareness in BoC

•

Provide direction to the CISO

•

Oversee all aspects related to security operations and drive overall information security in BoC

Information Security Unit -

Key Activities

•

Development, maintenance and implementation of the ISP of the Bank and overseas branches

•

Comprehensive risk assessments on overall operations and products

•

Management of Information Security

incidents

•

Improvements to the current information security infrastructure

•

Compliance with legal/regulatory requirements /standards

•

Strengthen Information Security awareness of employees and customers through various channels

•

Being resourceful in procurement related meetings to ensure that products are in compliance with the Bank’s security requirements

IT Risk Unit - Key Activities

•

Assess the risk of system requirements, newly-developed systems and changes done for existing systems

•

Development, maintenance, and implementation of IT Risk Policy of the Bank including overseas branches

•

Strengthening IT Governance

Policies

•

Information Security Policy

•

Cyber Security Policy

•

Vulnerability Management Policy

•

IT Risk Management Policy

•

Overseas Branches Cyber Security Policies, IT Risk Management Policies and Information Security Policies

STRATEGIC RISK

This involves the potential losses arising from the possible flaws in the Bank’s future business plans and the possibilities of strategies being inadequate. Formulating proper response plans to refine the Bank’s strategy to suit the changes in the business environment is essential for management of strategic risk.

The strategic direction of the Bank provided by its overarching vision and mission, articulated in BoC’s corporate plan with specific measurable time- bound targets. The Bank’s strategic plan is developed under the guidance of Board of Directors and the involvement of the Corporate Management and Executive Management team taking into consideration the changes in the operating context and stakeholder needs. Continued monitoring of performance is carried out against defined targets and comprehensive scorecards are used to measure strategic risk exposures.

KEY DEVELOPMENTS IN 2023

•

The Strategic Plan (SP) of the Bank was developed for five year time horizon intensifying the strategic direction and enabling the Bank to formulate a wide- ranging plan for accomplishing objectives of its stakeholders. A special committee appointed by the corporate strategic review committee studied the changes for repositioning the business model of the bank for next five years.

Opportunities

•

The gradual recovery of the economy complemented by the monetary policy easing will enable the counterparties to meet their debt obligations meeting Bank's asset quality targets. With the continuous support by the International Monetary Fund (IMF) in rebuilding the economy and restructuring process the recapitalisation targets will be achieved.

Opportunities

•

Establish a data protection unit to strengthen the IT governance framework

•

Partner with fintechs and value- added service providers to expand our product range and customer reach

•

Align processes and frameworks with the internationally recognised COBIT 2019 framework

HUMAN RESOURCE RISK

Continued challenging economic environment and socio-political conditions poses a pressure on the human capital of the Bank resultant high staff turnover and challenged talent acquisition. In this context, the Bank placed heavy emphasis on employee well-being, training and development as well as recognising and rewarding performance to strengthen and equip the Bank’s employees to function at their optimum.

KEY DEVELOPMENTS IN 2023

•

The Bank managed the talent acquisition through new recruitments of management trainees and staff assistants

•

Introduction of new human resource related policy frameworks and reviewing of existing policies to accommodate the changing requirements of the human capital management

•

Continuous employee development programmes

•

The pilot run on distance working has been a success within the Bank enabling flexible working hours without compromising the service level

•

Flexibility in employee dress code is also a key milestone in the human capital management history

•

Appointed a Data Protection Officer in line with the enactment of the Privacy Data Protection Act No. 9 of 2022

•

Conducted rigorous information security awareness and training

REGULATORY AND

COMPLIANCE RISK

Regulatory and compliance risk arises from the failure to comply with laws, regulations, and industry standards governing banking activities. In 2023, the Bank continued to navigate a complex regulatory environment, including prudential regulations, Anti- Money Laundering (AML) requirements, consumer protection laws, and international standards through close and proactive engagement with regulators. A dedicated Compliance Unit monitors all compliance with guidelines and regulations. A comprehensive compliance policy governs the compliance risk management. Continuous island-wide training and awareness programmes and onsite compliance assessments including overseas branches ensure effective management of regulatory and compliance risk.

KEY DEVELOPMENTS IN 2023

•

Implemented system developments for compliance reporting requirements

•

Carried out island-wide training programmes

•

Onsite compliance assessment

CLIMATE RISK

Climate-related risks including natural disasters and failure to implement long- term climate adaptations and solutions, are among some of the key risks faced by the Bank and its stakeholders. Addressing climate risk requires us to integrate climate considerations into our risk management frameworks, strategic planning processes, and decision- making practices. This includes assessing and disclosing climate-related risks and opportunities, implementing risk mitigation strategies, and engaging with stakeholders to promote sustainable finance and resilience-building efforts. By proactively managing climate risk, BoC aims to enhance its resilience, protect financial interests, and contribute to the transition to a low-carbon, climate- resilient economy.

A dedicated unit has been set up under the CFO, and an AGM has been appointed to manage the ESG aspect of the Bank. Board approved policies and procedures have also been implemented in terms of climate risk management. Extending the Bank commitment along the value chain, the Bank carries out prudent and careful evaluation of credit facilities above LKR 25 million to grant environmental and social clearance in compliance with the ESG principles of the Bank.

KEY DEVELOPMENTS IN 2023

•

Converted 52 branches to solar energy. All Bank owned buildings are to be converted by 2024.

•

Successful island-wide roll-out of the Environmental and Social Management System (ESMS) to assess environmental and social risks of the lending portfolio of the Bank.

•

Carried out training programmes on ESMS to develop a holistic approach to investment analysis, which incorporates environmental and social consideration.

Opportunities

•

Introduce sustainable lending products

•

Strengthen correspondent banking relationships with international funding agencies

LEGAL AND

REPUTATIONAL RISK

Legal and reputational risk entails potential losses to earnings and reputational damage arising from non- compliance with regulatory/statutory provisions, uncertainty due to legal actions, or uncertainty in the applicability or interpretation of relevant laws or regulation applicable to the Bank and negative perception of the stakeholders on Bank's financial and operation position.

RISKS AND OPPORTUNITIES

Opportunities

•

The continuous effort on complying with the Sustainability Road Map of CBSL, the Bank carries out environmental-friendly Corporate Social Responsibility (CSR) projects which will enhance the reputation of the Bank.

KEY DEVELOPMENTS IN 2023

•

Strengthen the customer complaint handling process through establishment of a separate customer complaint handling unit.

•

Increased usage of social media has widened the vulnerability to reputation risk. The establishment of a separate unit for social media response handling has contributed successfully in managing negative response on Bank on social media.