STRATEGY AND RESOURCE

ALLOCATION

Excellence

in Customer

Experience

Digital

Excellence

Rewarding Credit

Culture and Healthy

Credit Portfolio

Building a

High-Performing

Team

Leveraging

our strengths

•

Extensive branch network

spread across the country

and large correspondent

banking network with

wide coverage.

•

Leading Banking brand in

the country

•

Market Leadership

Addressing

our weaknesses

•

Attracting new generation

•

Risk of Stage 3 loans

exposures.

•

Legacy systems

and challenges in

integration.

Identifying

opportunities

•

Increase in digital adoption

•

Tendency for green

financing

•

Credit demand in line with

the boom in economic

activities

Safeguarding

against threats

•

Competition from peers and

fintech companies

•

Cyber security threat

•

Implications of climate

changes

•

Brain drain

I n t e n d e d o u t c o m e s :

Unlocking

value by

S

T

W

O

Excellence in

customer service

Ensuring consistent

and superior customer

experience across all

brick and mortar, and

virtual platforms.

Retaining market

leadership

Leverage the Bank’s brand

strength and unmatched

customer expectations,

offer relevant products

and superior customer

experience, to maintain

market leadership position.

Leading in digital

adoption

Transforming the

experience of both

internal and external

customers by adopting

cutting-edge technology

Best in sustainable

banking

Effectively address

challenges prevalent in

the economic, social and

environmental spheres

by deploying proactive

and meaningful solutions

Strategic

pillars:

Growth

Stability,

Governance

and Sustainable

In a landscape defined by economic dynamism and technological evolution, BoC stands at the

forefront, poised to redefine the future of banking. Our strategy is not just a roadmap; it's a

commitment to innovation, customer centricity, and sustainable growth. This section outlines

the key pillars of our strategic framework and the actionable steps we are taking to drive

growth and prosperity for all citizens.

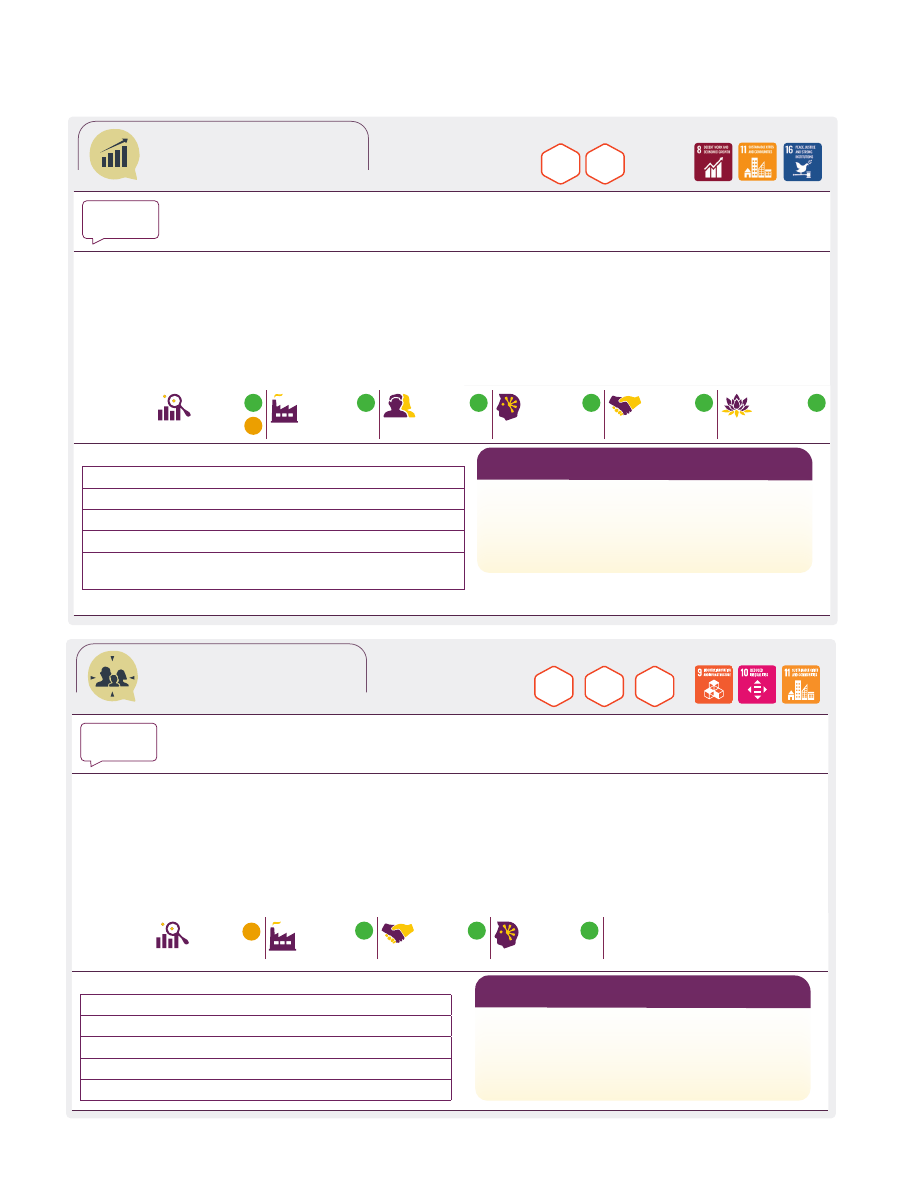

Excellence in

Customer Experience

Related SDGs:

Related material themes:

M1

M2

M4

WHY IT

MATTERS

Our customers are at the core of everything we do. Thus, we are committed to understand their evolving needs

and preferences to deliver personalised solutions that, cater to their financial goals.

RESOURCE ALLOCATION

•

LKR 3.2 billion investment in property, plant and equipment

•

42 branches refurbished

•

35 training programmes conducted on customer service

•

1,210 customer awareness programmes conducted

•

Various concession to customers in terms of rescheduling and

restructuring

CAPITAL TRADE-OFFS

•

Financial capital was impacted due to deferment of

payments, interest rate reductions etc.

•

These actions helped retain our customers and

strengthened our brand image.

•

Improvements to the customer contact points

strengthened our footprint across the island.

Capital

impacted

Financial

Capital

-

Manufactured

Capital

+

Social and

Relationship

Capital

+

Intellectual

Capital

+

2023 OUTCOMES

Net Promoter Score (NPS)

33%

Customer Satisfaction Score (CSAT)

79%

New customers acquired

1,045,000

Customer penetration

73%

Customer touchpoints

2,241

2024 FOCUS

•

Improve the turnaround time

•

Introduce products that appeal to the younger

generation

Stability, Governance

and Sustainable

Growth

Related SDGs:

Related material themes:

M2

M4

WHY IT

MATTERS

Prioritising stability, governance and sustainable growth builds the trust and loyalty of our stakeholders, ensures

ethical operations, and secures a lasting impact on the community and the environment.

RESOURCE ALLOCATION

•

USD 3.0 billion allocated to finance essential imports

(fuel and gas)

•

LKR 129.7 million investment in community engagement

•

52 solar-powered branches as of end 2023

•

1,126 officers trained for ESMS screening

CAPITAL TRADE-OFFS

•

Allocation of capitals to mainstream sustainable growth

and align with the CBSL’s Sustainable Financing roadmap

has in turn led to improved brand presence and equity; a

better-equipped workforce; improved relationships with

business partners, regulators, and communities and a

positive environmental impact.

Capital

impacted

Financial

Capital

-

+

Manufactured

Capital

+

Human

Capital

+

Intellectual

Capital

+

Social and

Relationship

Capital

+

Natural

Capital

+

2023 OUTCOMES

Economic value created

LKR 144.1 billion

Carbon footprint reduction

28%

Renewable energy generated

3,245.3 MWh

Scholarships to Nanajaya beneficiaries

2,872

Hapana Grade 5 scholarships for Ran

Kekulu account holders

12,459

2024 FOCUS

•

Sustain the market leadership

•

Accelerate the operations of overseas branches

•

Enhance sustainability engagements

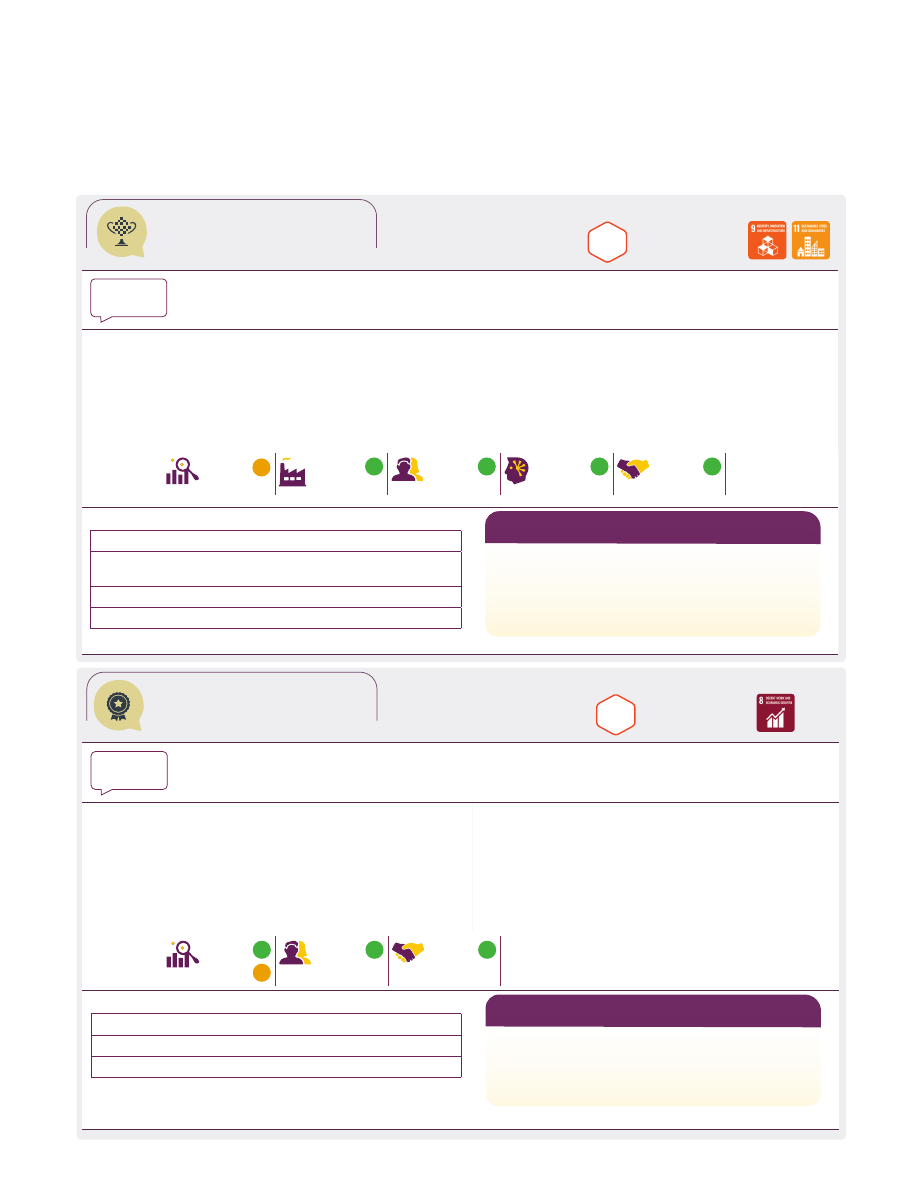

Rewarding Credit

Culture and Healthy

Credit Portfolio

Related SDGs:

Related material themes:

M2

WHY IT

MATTERS

A healthy credit portfolio is synonymous with financial stability. It reflects the quality of assets and the Bank's

ability to manage credit risk effectively.

RESOURCE ALLOCATION

•

LKR 3.4 billion credit concessions granted

•

58 training programmes conducted

•

LKR 38.8 billion of customer cash flow managed by BRRU

•

21 recovery workshops conducted

•

174 customers were supported under BRRU

CAPITAL TRADE-OFFS

The Bank prioritised the revival and rehabilitation of

businesses, as part of its customer-centric approach by

allocating both financial capital and human capital.

Capital

impacted

Financial

Capital

-

+

Human

Capital

+

Social and

Relationship

Capital

+

2023 OUTCOMES

Loan book value

LKR 2.5 trillion

Stage 3 ratio

5.1%

Number of customers revived

174

2024 FOCUS

•

Reduce Stage 3 loans and advances

•

Increasing private sector lending

•

More focus for green lending

Digital

Excellence

Related SDGs:

Related material themes:

M1

WHY IT

MATTERS

In an era where convenience is paramount, we believe in leveraging cutting-edge technology to enhance

customer experience, streamline operations, and introduce innovative financial products and services.

RESOURCE ALLOCATION

•

LKR 1.4 billion investment in digital infrastructure

•

163 CRMs installed

•

1,026 new POS machines

•

156 new IPG merchants

CAPITAL TRADE-OFFS

•

Investments were made to further strengthen the Bank's

digital infrastructure including cybersecurity.

•

These investments generate cost savings, improve

revenue streams, enhance customer experience and

unlock process efficiencies.

Capital

impacted

Financial

Capital

-

Manufactured

Capital

+

Human

Capital

+

Intellectual

Capital

+

Social and

Relationship

Capital

+

2023 OUTCOMES

Growth in digital transactions volume

8%

Customers onboarded to virtual

platforms

778,427

Digitally enabled customers

34%

Virtually enabled customers

19%

2024 FOCUS

•

Process streamlining

•

Data driven culture

•

Enhance digital adoption in rural areas

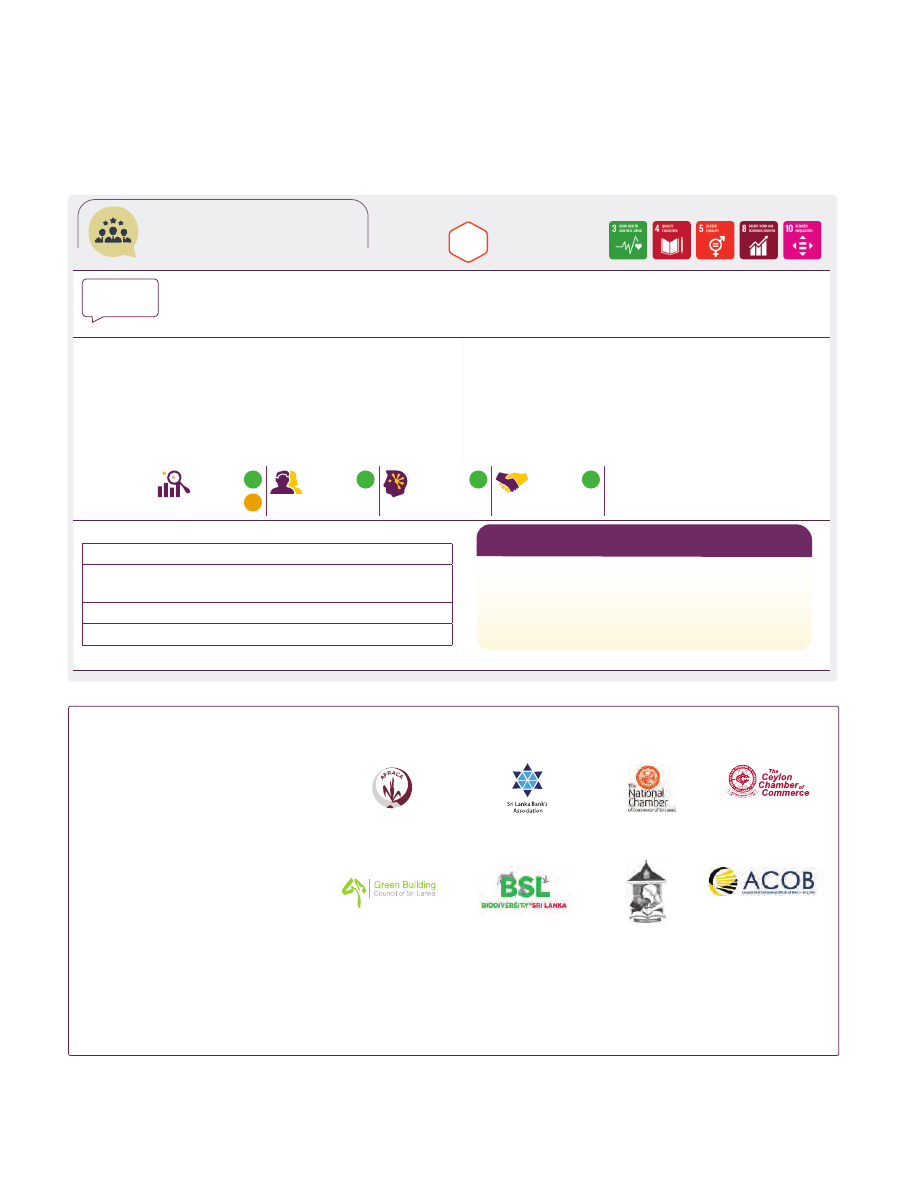

Building a

High-Performing

Team

Related SDGs:

Related material themes:

M3

WHY IT

MATTERS

We believe our people-centred corporate culture differentiates us in the market. We are focused on embracing

diversity and improving equality and inclusion in our workforce as this drives diversity of thought, innovation and

creativity needed in the future place of work.

RESOURCE ALLOCATION

•

LKR 29.8 billion invested in remuneration and benefits

•

LKR 200.1 million invested in training and development

•

LKR 183.4 million invested in staff safety and well-being

CAPITAL TRADE-OFFS

•

Among other benefits, financial capital was allocated to

adjust remuneration in line with the rising cost of living

and loans and advances at concessionary rates. Such

investments have enabled us to enhance employee

loyalty, greater customer service/experience, and results

in greater productivity and efficiency.

Capital

impacted

Financial

Capital

-

+

Human

Capital

+

Intellectual

Capital

+

Social and

Relationship

Capital

+

2023 OUTCOMES

Retention rate

95%

Average training hours per

employee

32 hours

Net profit per employee

LKR 3.1 million

Female representation

60%

2024 FOCUS

•

Improve productivity

•

Human Resources of the Bank ready for the virtual

environment

•

Increase employee well-being

STRATEGY AND RESOURCE

ALLOCATION

SUPPORTING FINANCIAL SERVICES

National Chamber of

Commerce, Sri Lanka

Ceylon Chamber of

Commerce

Green Building Council

of Sri Lanka

Biodiversity Sri Lanka

The Financial

Ombudsman of

Sri Lanka (Guarantee)

Limited

Sri Lanka Law Library

Asia Pacific Rural and

Agricultural Credit

Association (APRACA)

Sri Lanka Banks’

Association (Guarantee)

Limited

Association of Compliance

Officers of Banks, Sri Lanka.

Association of Banking

Sector Risk Professionals,

Sri Lanka

As one of the leading banks in the

country, BoC actively collaborates

with industry stakeholders through its

membership in industry associations

and professional bodies. The Bank's

membership in these institutes

contributes to the development

of industries, the financial services

sector and the Sri Lankan economy.

The Bank's membership in these

associations is an opportunity to

harness strength and partnership for

the mutual benefit of the industry.

During the year under review, the

Bank retained the membership of the

institutions including;