MATERIAL MATTERS

Our materiality determination process is carried out on an annual basis, to review and evaluate issues that are of material importance

to the Bank. These issues include events occurred in the Bank’s operating landscape during the year under review, which could

significantly affect our ability to achieve our strategic ambitions and to create value over the short, medium and long term.

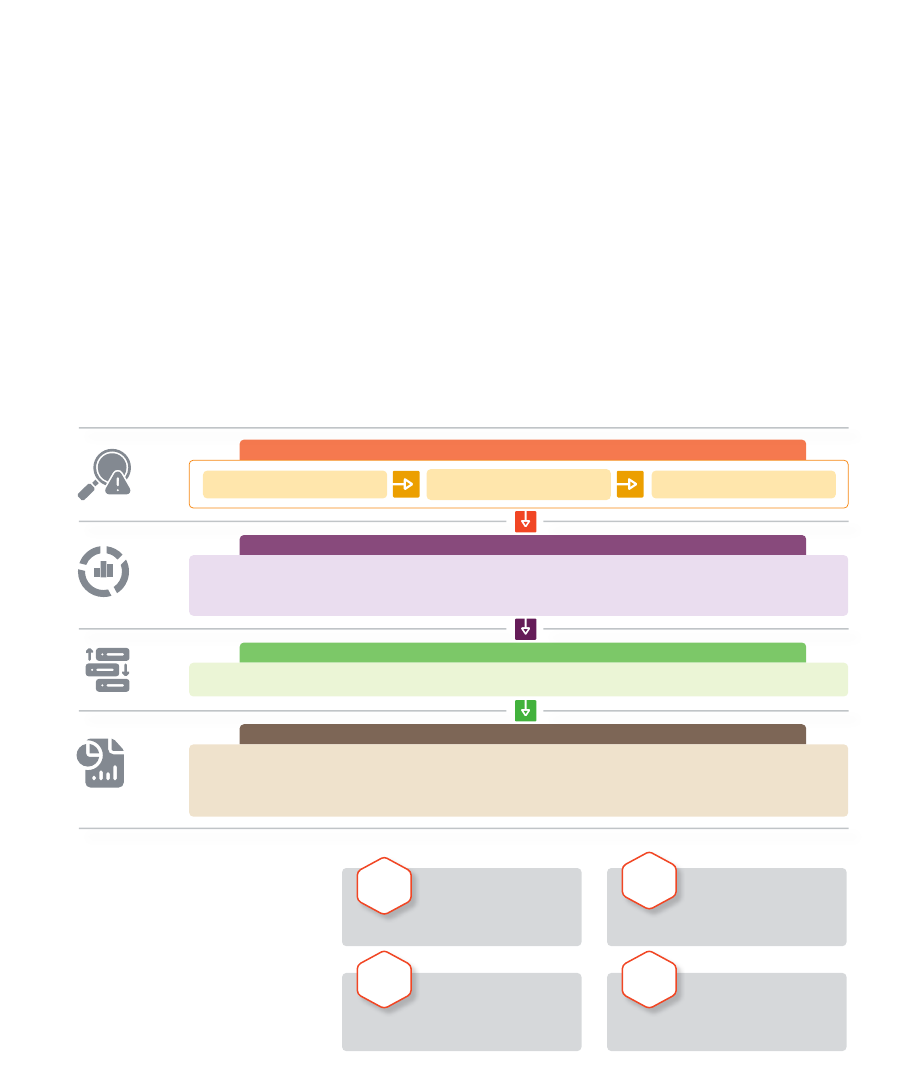

We follow a structured process to identify material topics that influence the Bank’s strategy and operations as outlined below.

OUR MATERIALITY DETERMINATION PROCESS

I D E N T I F Y

A S S E S S

P R I O R I T I S E

M O N I T O R A N D R E P O RT

We assess the relative importance in terms of the impact on the Bank’s strategy and

influence on stakeholder decisions

We continuously monitor the identified material topics taking account of changes in the operating

environment and respond by re-aligning the Bank’s strategy. Topic progress is reported to stakeholders

and the Board of Directors on a regular basis.

Material issues are ranked based on their likelihood and impact

The Operating Landscape

Stakeholder Needs and

Expectations

Risks and Opportunities

OUR MATERIALITY THEMES

The materiality assessment for 2023 was

built on the material topics identified

during the previous year and this year, we

grouped these topics under four broader

themes. The topics were reviewed in

line with changes in operations and

there were no significant changes to the

reporting boundaries. Further, there was

no change in materiality for the material

matters concerned.

M1

Adapting to the

evolving context

Caring for our

people

Enabling

responsible growth

Nurturing a

sustainable business

operation

M2

M4

M3

In line with the principle of double materiality, our Integrated Report extends beyond financial

reporting and includes non-financial performance, risk and opportunities and outcomes

attributable to or associated with our key stakeholders, which have a significant influence on

our ability to create and preserve value, while minimising value erosion.

A

M2 - 6 Responsible banking

M4 - 3 Climate change and environmental

footprint

B

M2 - 3 Responsible procurement

C

M3 - 3 Diversity and equal opportunity

D

M1 - 1 Macroeconomic developments and

policy trends

M1 - 2 Customer experience

High

High

Low

Low

F I N A N C I A L M A T E R I A L I T Y ( I N T E R N A L )

IMP

ACT MA

TERIALITY (EXTERNAL)

C

A

B

D

M1 - 3 Customer privacy and data security

M1 - 4 Digitalisation and technology

M2 - 1 Customer support and business

revival

M2 - 2 Brand reputation

M2 - 4 Anti-bribery and anti-corruption

M2 - 5 Regulatory environment,

governance, and compliance

M3 - 1 Employee health, safety and

wellbeing

M3 - 2 Talent management and labour

relations

M3 - 4 Labour rights (outsourced/contract)

M4 - 1 Financial performance

M4 - 2 Socio-economic contribution and

financial inclusion

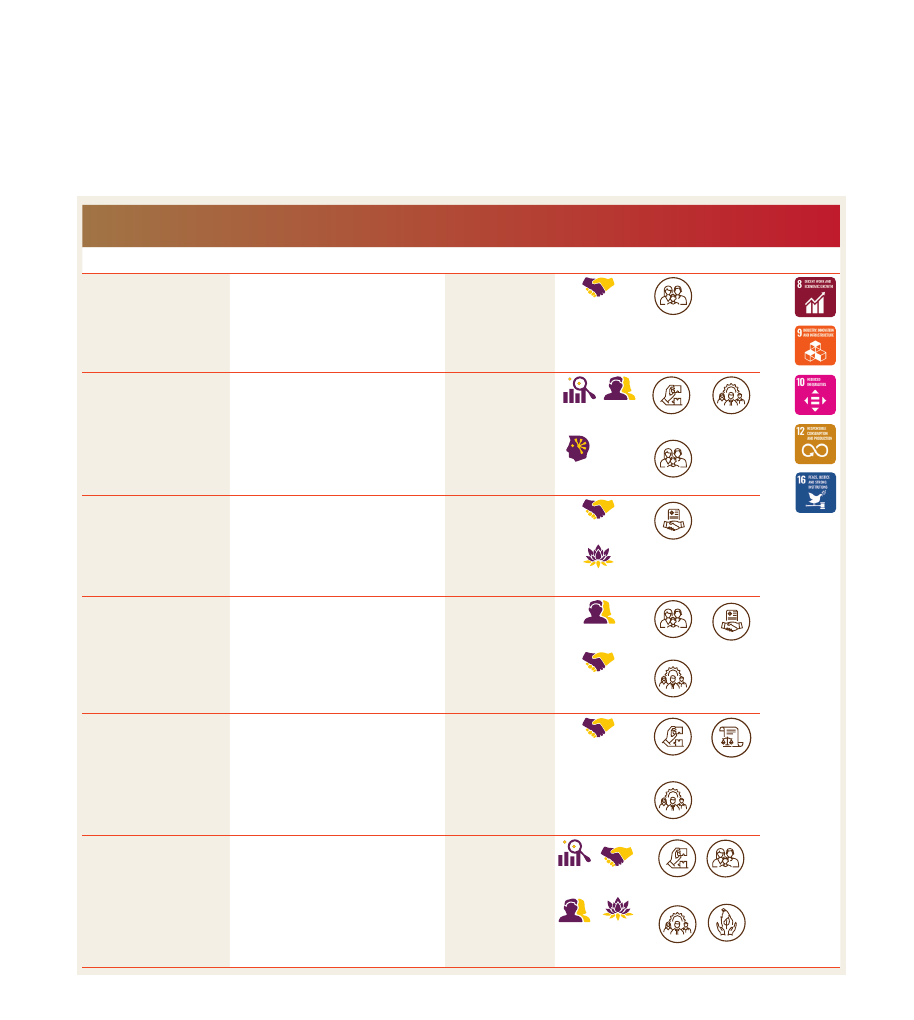

MATERIAL MATTERS

Material

topics

Why it is

material to BoC

Our response

Capitals

impacted

Stakeholders

impacted

Contribution

to UN SDGs

M1 : Adapting to the evolving context

1 Macroeconomic

developments and

policy trends

Multifaceted challenges affecting

Sri Lankan economy and related policy

developments have a direct impact

on the financial sector operations,

performance and sustainability.

The operating

landscape

Pages 44 to 48.

Financial

Capital

Manufactured

Capital

Customers

Shareholder and

Fund Providers

Employees

2 Customer

experience

The key differentiator in the intensely

competitive banking sector of

Sri Lanka.

A primary partner

for our customers

Pages 84 to 89.

Social and

Relationship Capital

Customers

3 Customer privacy

and data security

(GRI 418 SASB FN-

CB-230a.2)

Increased thrust towards digitalisation

has heightened vulnerability to

customer privacy and security issues,

thereby requiring organisations to

strengthen IT security frameworks.

A digitally

empowered Bank

Pages 98 to 102.

Social and

Relationship Capital

Customers

4 Digitalisation and

technology

Driving digital excellence is a key

strategic aspiration for the Bank.

A Digitally

Empowered Bank

Pages 98 to 102.

Manufactured

Capital

Customers

Employees

Material

topics

Why it is

material to BoC

Our response

Capitals

impacted

Stakeholders

impacted

Contribution

to UN SDGs

M2 : Enabling responsible growth

1 Customer support

and business revival

(SASB FN-CB-240a.1

SASB FN-CB-240a.2)

We continue to lead the country’s

economic recovery by supporting

business revival through rescheduling/

restructuring facilities, cash flow

monitoring and providing access to

finance.

A primary partner

for our customers

Pages 84 to 89.

Social and

Relationship Capital

Customers

2 Brand reputation

Consistently ranked as Sri Lanka's

No.1 banking brand, and Positive

brand and reputation help to attract

and retain customers and other

stakeholders.

A primary partner

for our customers

Pages 84 to 89.

Intellectual

Capital

Financial

Capital

Human

Capital

Customers

Shareholder and

Fund Providers

Employees

3 Responsible

procurement

(GRI 204)

BoC engages with a large base of

suppliers and ensures responsible

practices in procurement through

propagation of sustainable practices.

A beacon of trust

in everything

we do

Pages 103 to 109.

Social and

Relationship Capital

Natural

Capital

Business

Partners

4 Anti-bribery and

anti-corruption

(GRI 205, 406 SASB

FN-CB-510a.2)

As a state-owned entity, nurturing a

culture of anti-bribery and

anti-corruption is vital in the

responsible creation of shared value.

A winning,

talented and

diverse team

Pages 90 to 97.

Human

Capital

Social and

Relationship Capital

Customers

Employees

Business

Partners

5 Regulatory

environment,

governance and

compliance

(GRI 207, 419, 307)

It is imperative to ensure compliance

on current and emerging regulations

as failure to do so leads to litigation,

regulatory and reputational risks.

Corporate

governance

Pages 111 to 121

Risk and

opportunities

Pages 132 to 148.

Social and

Relationship Capital

Shareholder and

Fund Providers

Employees

Regulators

6 Responsible

banking

Responsible lending practices

underpin BoC’s ability to drive

impactful socio-economic change.

Performance of

business segments

Pages 73 to 82.

Financial

Capital

Human

Capital

Social and

Relationship

Capital

Natural

Capital

Customers

Shareholder and

Fund Providers

Employees Community and

Environment

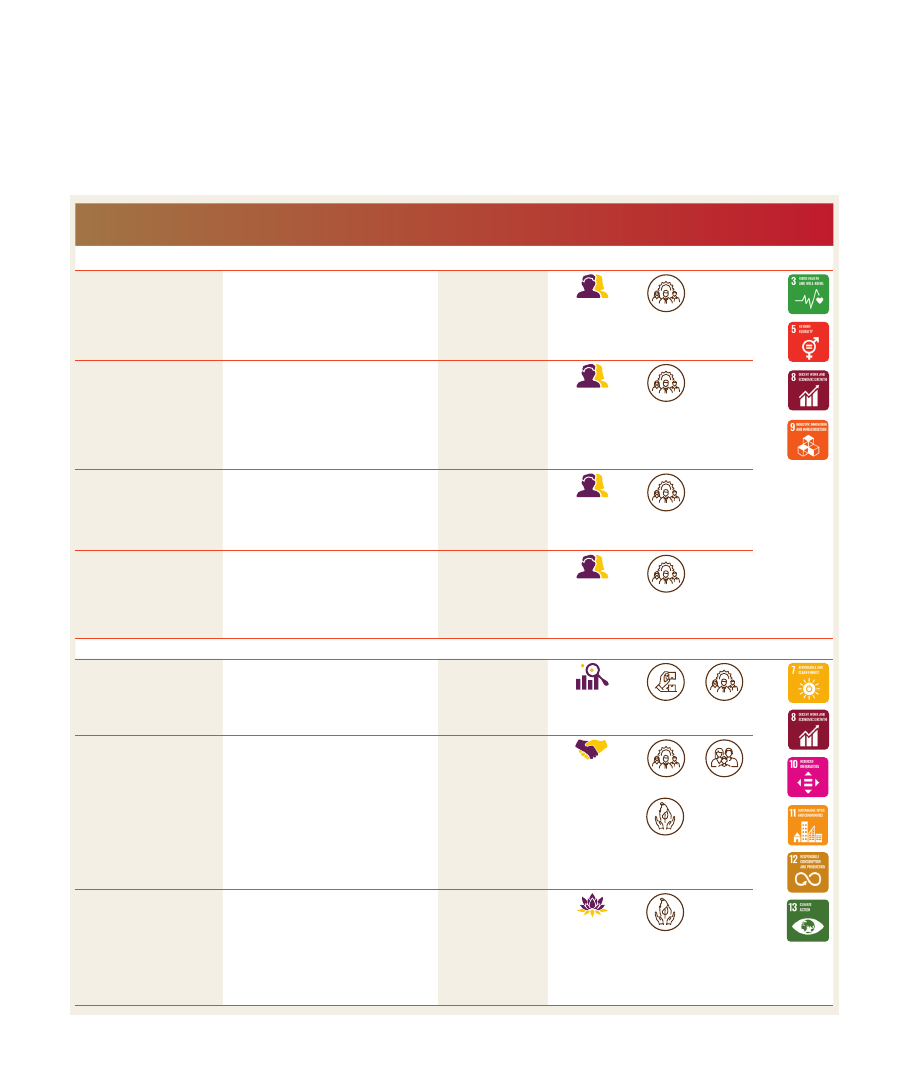

Material

topics

Why it is

material to BoC

Our response

Capitals

impacted

Stakeholders

impacted

Contribution

to UN SDGs

M3 : Caring for our people

1 Employee health,

safety and wellbeing

(GRI 403)

Promoting employee health,

safety, and well-being enhances

employee productivity and minimises

absenteeism, employee turnover and

hiring costs.

A winning,

talented and

diverse team

Pages 90 to 97.

Human

Capital

Employees

2 Talent management

and labour relations

(GRI 401, 402, 404,

407)

Employees are vital in driving

corporate strategy and are one of

the Bank’s most valuable assets,

underscoring the importance of

managing employee related issues

effectively.

A winning,

talented and

diverse team

Pages 90 to 97.

Human

Capital

Employees

3 Diversity and equal

opportunity

(GRI 405)

Prioritising diversity creates a positive

work environment that supports

the overall goals of the Bank and

contributes to its long-term success.

A winning,

talented and

diverse team

Pages 90 to 97.

Human

Capital

Employees

4 Labour rights

(outsourced/

contract)

(GRI 408, 409)

BoC is committed to provide a safe

and conducive work environment

for all outsourced and contract

employees engaged by the Bank in

addition to the permanent cadre.

A winning,

talented and

diverse team

Pages 90 to 97.

Human

Capital

Employees

M4 : Nurturing a sustainable business operation

1 Financial

performance

(GRI 201)

Critical in ensuring commercial

sustainability and continued value

generation to stakeholders.

Financial review

Pages 68 to 72.

Financial

Capital

Shareholder and

Fund Providers

Employees

2 Socio-economic

contribution and

financial inclusion

(GRI 201, 202, 413,

203

SASB N-CB-240a.3

SASB FN-CB-240a.4)

Promoting socio-economic

empowerment and financial

inclusion open access to new

markets, generates new revenue

streams, improves reputation

and also contributes to economic

development.

A beacon of trust in

everything we do

Pages 103 to 109.

Embedding

sustainability

Pages 61 to 63.

Social and

Relationship Capital

Community and

Environment

Employees

Customers

3 Climate change

and environmental

footprint

(GRI 302, 305

SASB FN-CB-410a.2)

Minimising the environmental

impact can help to meet regulatory

requirements, enhance reputation,

reduce costs, increase revenue and

create new business opportunities.

A beacon of trust

in everything

we do

Pages 103 to 109.

Natural

Capital

Community and

Environment

MATERIAL MATTERS