THE OPERATING

LANDSCAPE

According to the World Economic

Outlook, the global economic growth

is projected to reach 3.1% in 2024.

Asia will likely to be the fastest-

growing region and will continue to

drive global growth, expanding by

5.4%. Among the major economies,

the United States is expected to

witness a mild contraction of 0.2%

in 2023, in the United Kingdom a

contraction of 0.5%, while the Europe

is likely to see an overall modest

expansion of 0.4%.

POLITICAL AND ECONOMIC

LANDSCAPE

GLOBAL CONTEXT

BoC continuously monitors the operating

environment using a PESTEL framework to

identify material risks and opportunities that

may affect its ability to generate value in the

short, medium, and long term. Following are

the critical factors that influenced the Bank's

performance and strategy during the year.

According to the World Economic

Outlook, the global economic growth

is projected to reach 3.1% in 2024.

Asia will likely to be the fastest-

growing region and will continue to

drive global growth, expanding by

5.4%. Among the major economies,

the United States is expected to

witness a mild contraction of 0.2%

in 2023, in the United Kingdom a

contraction of 0.5%, while the Europe

is likely to see an overall modest

expansion of 0.4%.

Global headline inflation is expected

to fall from 6.8% in 2023 to 5.2% in

2024. Price pressures are still elevated

in many countries and any further

escalation of geopolitical conflicts

in the Middle East poses a threat to

increase in inflation.

After facing an extremely challenging period in 2022, Sri Lanka has

demonstrated resilience and stability, on many economic fronts, as a result

of timely implementation of effective macroeconomic policies and structural

reforms.

Domestic economic activity, which saw a contraction in the first quarter of 2023

has rebounded, supported by the easing of monetary conditions and growth

supportive policies implemented by the GOSL, enabling the domestic economy

to achieve sustainable levels of growth.

After reaching a peak of 73.7% headline (consumer) inflation in 2022, Sri Lanka

is witnessing a gradual moderation of prices, with a reduction in aggregate

demand, boosts in local supply-chain production, and a normalisation of global

commodity prices, which has all led to the dis-inflationary process.

A stabilisation of domestic inflation is expected to enhance the purchasing

power of economic agents and improve their debt repayment capacities.

As Sri Lanka recovers from a tough year, the Rupee in 2023 showed signs of

gradual appreciation. This signals for judicious planning to steer the country

towards sustained economic growth.

Sri Lanka’s official reserves stood at USD 3.7 billion in November and exceeded

USD 4.3 billion in December 2023 - the highest level since the country plunged

into an economic crisis.

Sri Lanka’s performance under the International Monetary Fund (IMF)

programme was satisfactory, providing the country with access to Special

Drawing Rights (SDR) in support of country’s economic policies and reforms,

leading to a restoration of debt sustainability, raising revenue, rebuilding

reserves buffers, reducing inflation, and safeguarding financial stability.

LOCAL CONTEXT

Receiving the first tranche and the anticipated second tranche of the IMF bailout package after meeting IMF conditions has

signaled to the international community that Sri Lanka is on its path towards economic recovery, and can re-establish its

economic heydays, as a trailblasing Asian nation.

BANKING INDUSTRY OUTLOOK

The banking sector remained resilient despite the contraction anticipated for 2023, which was less severe with the gradual

easing of the monetary policy. Macro-economic policy reforms are bearing fruit, and the economy is showing tentative signs of

stabilisation.

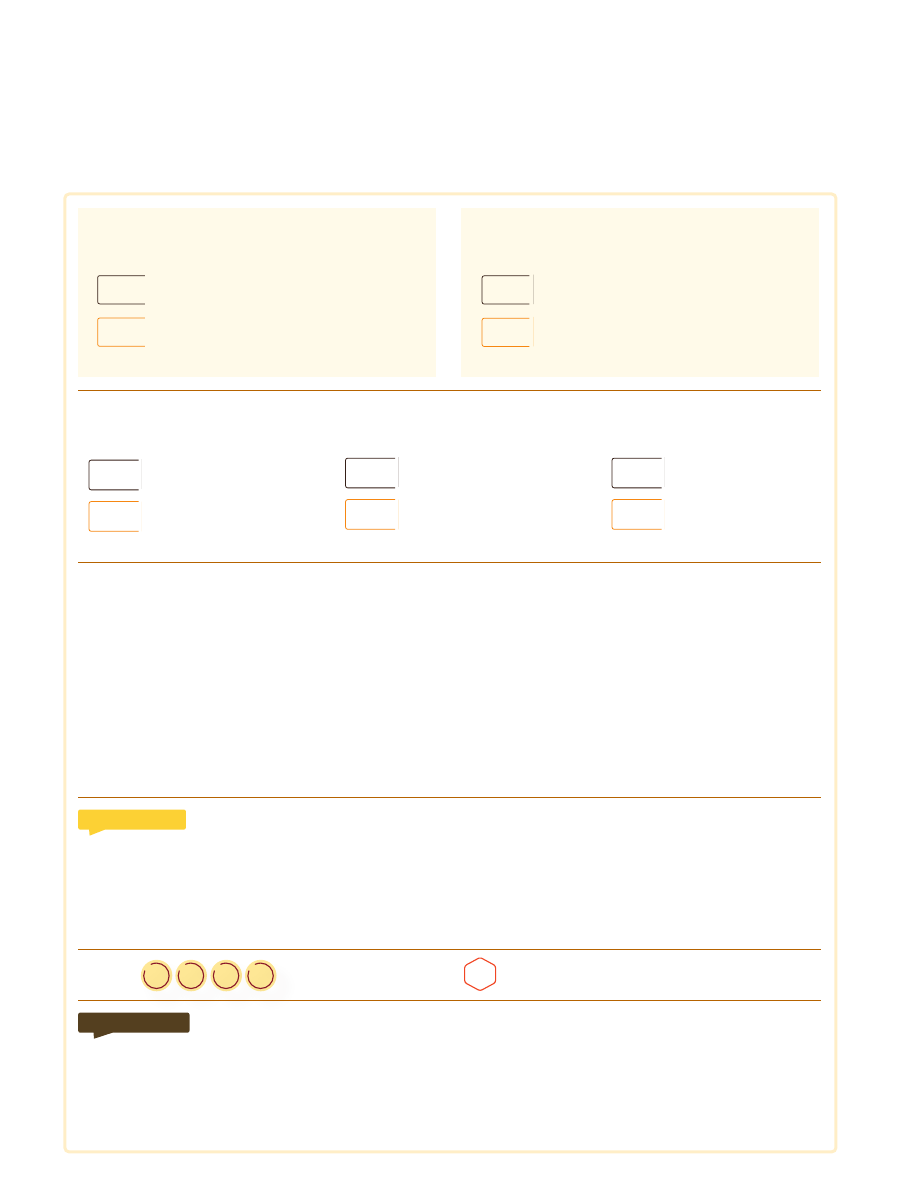

ASSET BASE

2023

20.4 trillion

19.4 trillion

2022

Total assets (LKR)

2023

11.0 trillion

11.3 trillion

2022

LENDING PORTFOLIO

Gross loans and advances (LKR)

QUARTERLY REAL GDP GROWTH

GDP Growth

-20

-15

-10

-5

0

5

10

15

20

INFLATION: Y-O-Y %

CHANGE IN CCPI AND NCPI

0

10

20

30

40

50

60

Jan-23

Feb-23

Mar-23

Apr-23

May-23

Jun-23

Jul-23

Aug-23

Sep-23

Oct-23

Nov-23

Dec-23

NCPI (2021=100)

CCPI (2021=100)

LENDING AND DEPOSIT RATES

0

5

10

15

20

25

30

Dec-22

Mar-23

Jun-23

Sep-23

Dec-23

AWDR

AWPR

Source: Central Bank of Sri Lanka

FUNDING

Deposits (LKR)

2023

16.6 trillion

15.3 trillion

2022

PROFITABILITY

Profit before tax (LKR)

2023

294.4 billion

177.8 billion

2022

The recovery of the Sri Lankan economy in the short to medium term depends on the successful continuation of the policy

reforms underpinned by the Extended Fund Facility (EFF) arrangement obtained from the International Monetary Fund (IMF).

This requires credible actions to improve fiscal performance and strengthen external sector buffers, while ensuring price

stability and financial system stability.

The gradual normalisation of market lending interest rates and improvements in investor and business confidence are

expected to support the expansion of credit to the private sector going forward.

To ensure that banks are adequately capitalised, the CBSL is in a stringent process of evaluation to identify the adequacy of

capital for future developments in banks. Furthermore, broad guidelines are expected to be issued by CBSL to strengthen the

role of licensed banks in the sustainable revival of businesses, especially Small and Medium Enterprises (SMEs) and corporates,

and to ensure the assets quality is maintained.

IMPACT TO BOC

•

The IMF-led domestic debt optimisation strategy as well as the restructuring of State-Owned Enterprises (SOEs) could

affect the banking sector balance sheet.

•

The benchmark interest rates were lowered for the first time in three years, creating opportunity for the growth of the loan

book.

•

Insufficient funds in the inter-bank market hampering inter-bank borrowing.

R1

R2

R3

R4

RELATED

RISKS

RELATED MATERIAL

THEMES

M1

OUR RESPONSE

•

Provided funds to major SOEs in energy and pharmaceutical sectors, considering the overall national interest.

•

Timely support to customers facing pressure in repaying their loans.

•

Strengthened our focus on preserving liquidity.

•

Reliance on predictive forecasts to prioritise commitments and ensure facilitation of essential imports.

THE OPERATING LANDSCAPE

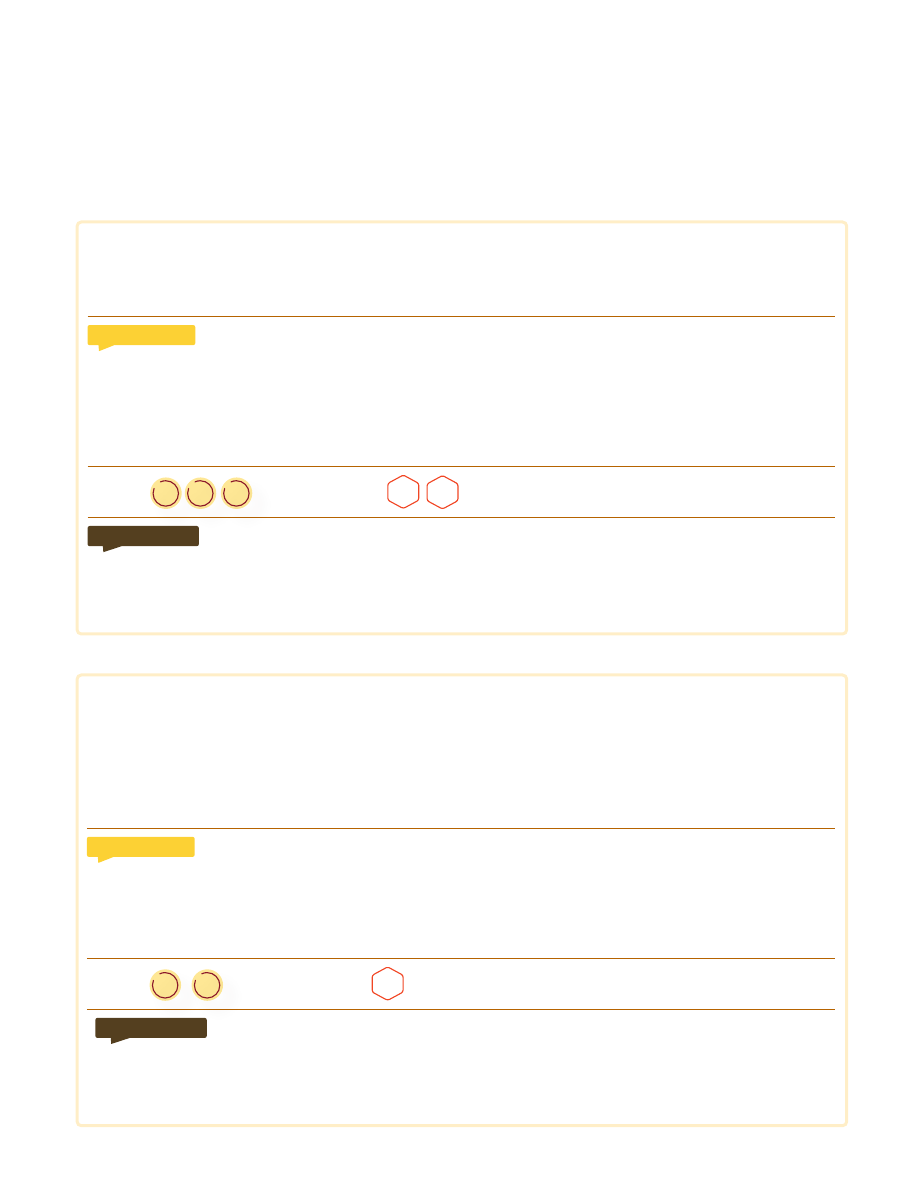

CAPITAL AND LIQUIDITY

Statutory Liquid Assets Ratio

Tier 1 Capital Ratio

Capital Adequecy Ratio

2023

46.7%

29.8%

2022

2023

13.8%

13.1%

2022

2023

16.9%

16.1%

2022

Source: Central Bank of Sri Lanka

THE EVOLVING SOCIAL CONTEXT

Sluggish economic growth, high inflation, and tax hikes have led to greater pressure on livelihoods, income and socio-economic

disparities. Vulnerable populations including the elderly, children, and persons with disabilities are particularly at risk of poverty

and social exclusion, requiring targeted social assistance and support mechanisms.

Outward migration also continued to grow particularly among the younger demographic, resulting in drain of skilled personnel.

IMPACT TO BOC

•

Increased credit risk due to reduced repayment capability of borrowers, resulting in adverse effects on portfolio quality.

•

Migration of skilled workers and the brain drain has led to high staff-turnover, resulting in a lack of employees with specialised

skills in the banking industry.

•

The flow of remittances increased during 2023, due to improved exchange rates and expatriates sending more

earnings, which has a positive impact on the Bank.

M4

R1

R4

R5

RELATED

RISKS

RELATED MATERIAL

THEMES

M3

OUR RESPONSE

•

The Bank did not curtail any financial or non-financial benefits to employees and took steps to match the Cost-of-Living

Allowance (COLA) in line with the rising inflation.

•

Supporting customer priorities and the needs of the Nation and enhanced customer loyalty.

DIGITAL TRANSFORMATION

Digital transformation in Sri Lanka continued to gain momentum, driven by technological advancements, changing consumer

behaviour, and Government initiatives to promote digitalisation across various sectors. The year witnessed the convergence of

Artificial Intelligence, Robotics, Cloud Computing and Big Data - influencing the country’s business and economic landscape.

A significant growth was also recorded in mobile and internet penetration rates, with a large percentage of the population

accessing the internet via smartphones and mobile devices. Technology companies are increasingly innovating in areas such as

digital banking, peer-to-peer lending, mobile payments, and remittances offering alternatives to traditional banking services,

promoting financial inclusion and driving efficiency in financial transactions and services.

IMPACT TO BOC

•

The digitalisation of financial services is transforming how banks operate. Hence, the Bank is in pursuit of improving its

processes through automations and system enhancements.

•

Alongside increased digitalisation the risk of cyber-attacks and fraud has also increased beckoning for tighter IT security

infrastructure.

R4

R5

RELATED

RISKS

RELATED MATERIAL

THEMES

M1

OUR RESPONSE

•

Improved digital penetration and digital literacy of the customer base.

•

Leveraged technology for increased process efficiencies and cost savings.

•

Strengthened IT security and governance protocols.

REGULATORY DEVELOPMENTS

The Bank operates in a highly regulated environment where new regulatory requirements were introduced frequently to

safeguard the stability of the financial sector including;

- Restricting discretionary payments of Licensed Commercial Banks (LCBs),

- Margin requirements against imports and maximum interest rates on certain lending products,

- Requesting LCBs to reduce the interest rates of lending products.

- Limitation in borrowings.

IMPACT TO BOC

•

Increased regulatory oversight and reporting.

•

Increased cost of compliance.

R1

R2

R4

R3

R5

RELATED

RISKS

RELATED MATERIAL

THEMES

M2

OUR RESPONSE

•

Adhered and complied with the Directions/ Guidelines issued by CBSL for LCBs and the circulars issued by Ministry of Finance.

•

Complied with the standards and guidelines issued by professional bodies and relevant institutions.

CLIMATE ACTION

As a small island and a developing nation, Sri Lanka is highly vulnerable to the adverse effects of climate change and the

consequences of climate change such as temperature rise, rainfall variability and sea level rise affect almost all economic sectors

of the country.

Sri Lanka’s Climate Prosperity Plan, which was launched at the U.N. Climate Change Conference in November 2022, aims to

stimulate climate protection and promote risk-informed investment with a commitment to developing a strategy of accelerated

adaptation of sectors most exposed to climate risks such as agriculture or fisheries, together with a comprehensive risk financing

strategy.

IMPACT TO BOC

•

As a Bank, we are under increasing pressure to address critical environmental issues facing the world today, and are required

to place emphasis on sustainable lending, emissions reduction strategies and climate adaptation and mitigation.

•

As customer awareness on environmental implications increases, there is greater expectation from multilateral and bilateral

lenders for responsible lending decisions that include social and environmental considerations.

R1

R4

R5

RELATED

RISKS

RELATED MATERIAL

THEMES

M4

OUR RESPONSE

•

Developed new banking solutions to address climate change related risks and support climate resilience.

•

Incorporated more green concepts into our sustainability agenda.

•

Continuously embedded social and environmental sustainability considerations into strategy and decision making.

•

Aligned our actions with the 17 SDGs to promote prosperity and protect the planet.

THE OPERATING LANDSCAPE